Yield Basis 2026 Thesis

In 2025, Yield Basis initiated the new Defi era of AMMs without Impermanent Loss.

All recent years Defi was developing with a focus to avoiding IL: there was no real solution, and all hedging options involve a lot of effort, cost, and risks.

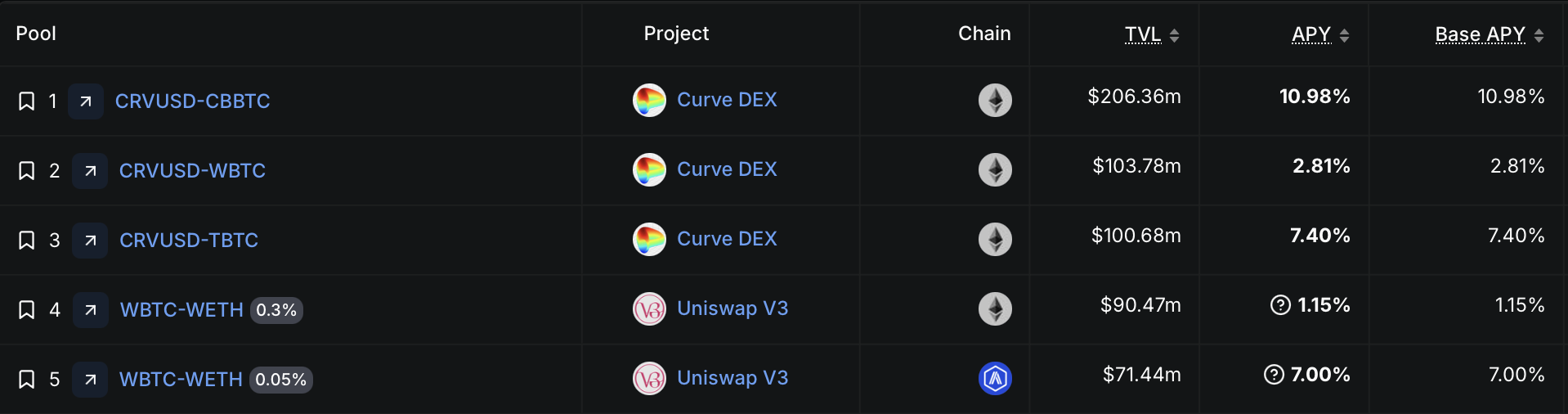

$ETH in Defi: No IL options: (top3 LST: $45B, ~2.5-2.8% APY, top3 lending: $13B, 0.01 - 1.17% APY), top1 Volatile ETH vs. stable pool: Uniswap v3 $104m, ~40% 30D APY.

Despite much higher formal APY, the option with IL risk has <<1% TVL of $ETH, deployed in other options. Almost nobody wants to risk ETH upside for AMM fees. Source: Defillama

In Yield Basis 2026 Thesis we explore 2025 YB performance & foreseeing evolution of the IL-free AMM protocol into a leading DeFi yield machine.

Yield Basis in 2025

#1: IL solution that really works

In 2025 Yield Basis proved: its leveraged AMM pool model eliminating impermanent loss (IL) is economically viable (the costs of eliminating IL are less than the profits):

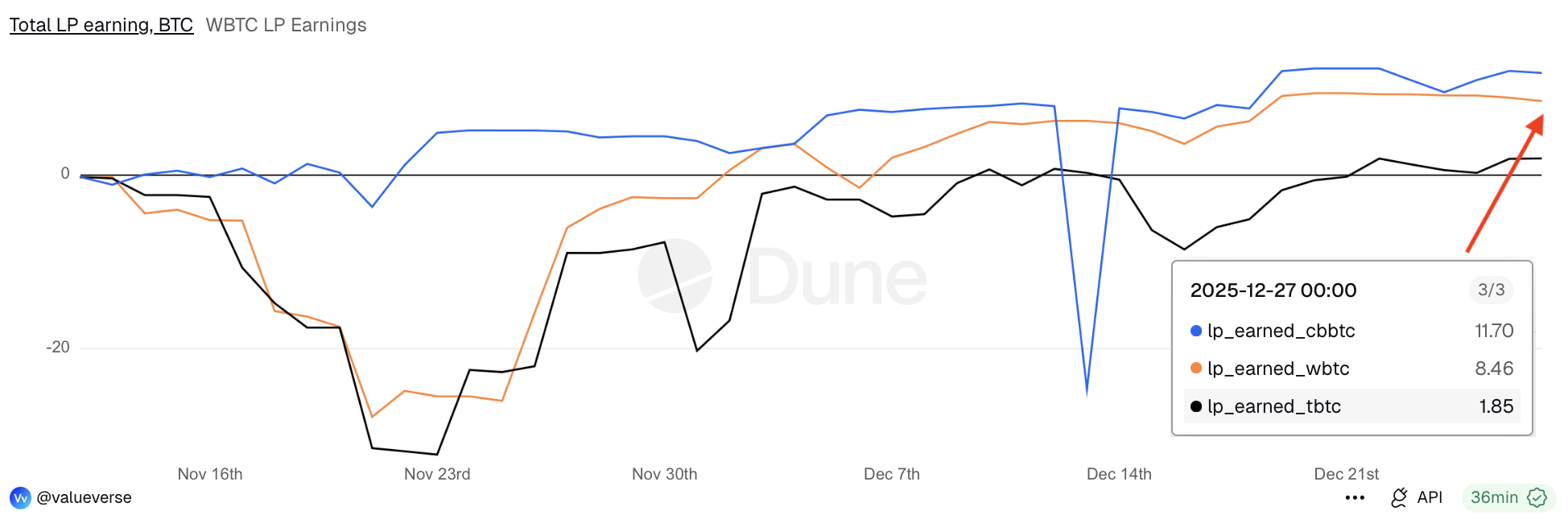

Table: LP APR & DAO income in 2025

| Pool (unstaked pools yielding BTC fees) | APR (accounting redemption value) |

|---|---|

| v1 pools LP yield | 16.11 BTC |

| v2 pools LP yield | 22.01 BTC (11.7 cbBTC, 8.46 wBTC, 1.85 tBTC) |

| Total (v1+v2) LP yield | 38.12 BTC |

| DAO (veYB) fees | $1,823,000 |

*realised and unrealised gains accounted

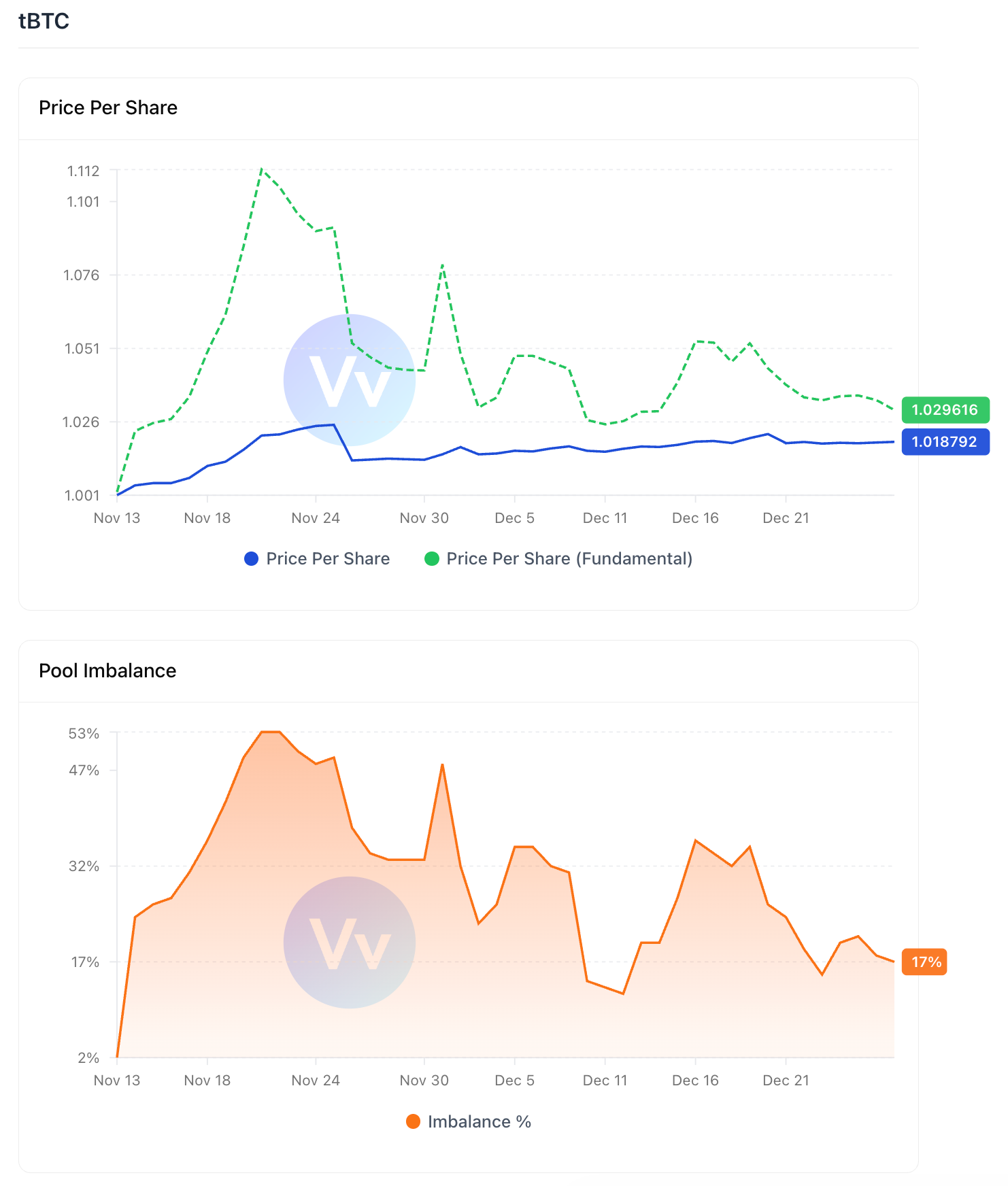

The poor tBTC performance is a result of inefficient arbitrage and related pool balancing due to redemption fees.

Below we provide comparison to redemption value & total LP profit vs. time for all three pools:

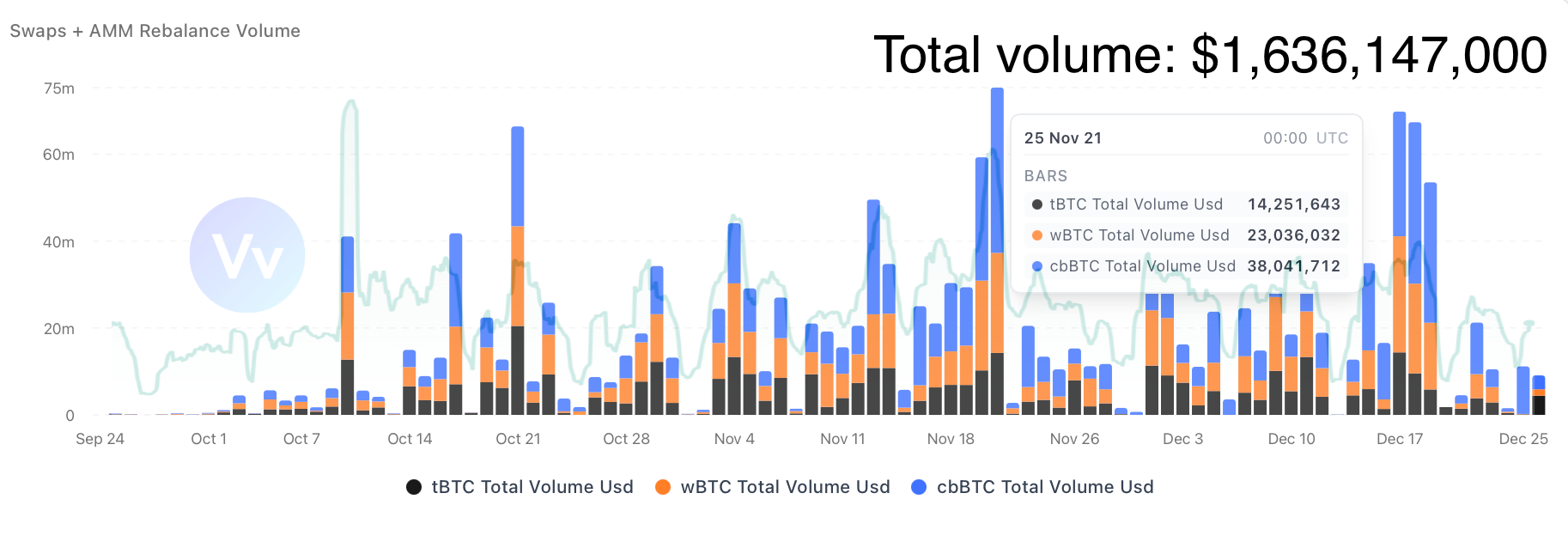

In 2025, Yield Basis processed more than $1.63B of trading volume, peaking during the high volatility (the green line is the BTC volatility index):

Yield Basis now accounts for the three largest Bitcoin pools in DeFi:

Source: Defillama

#2: The value of veYB

At the moment of YB emission launch, veYB (the locked YB version, that enables token utility) had only governance power influencing YB emissions distribution & protocol upgrades.

The Fee Switch event on 4th of December enabled the fully-pledged closed economic loop for the token. Now, its utility consists of Fees & Governance value that requires locking in a vote-escrow contract to be activated (not locked YB has no utility functions).

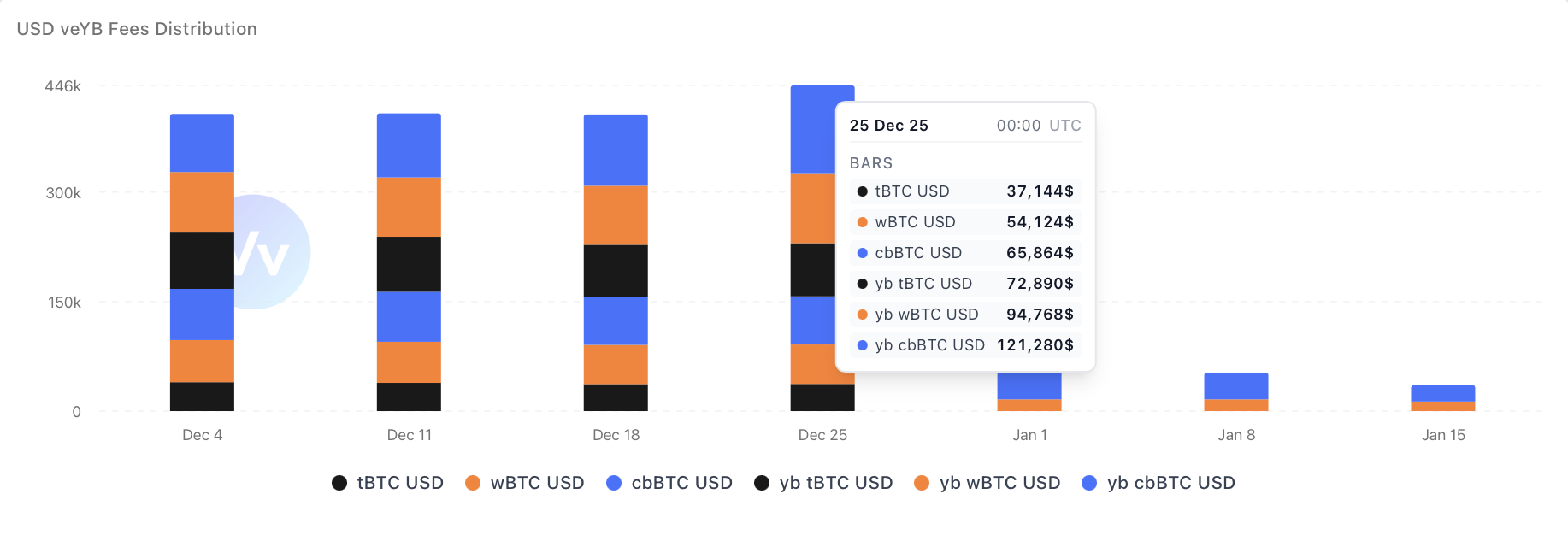

At 25th Dec the record fee distribution was processed, distributing ~450k in a single week:

Source: Valueverse

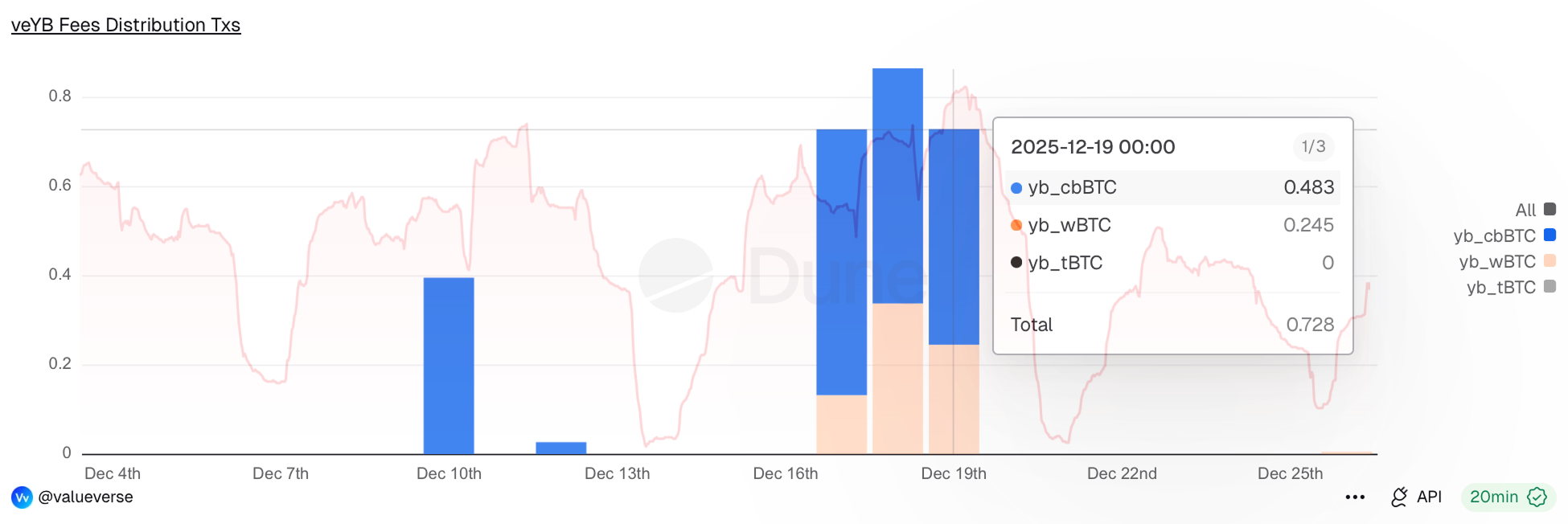

After pools migration, fees are collected in ybBTC what means that veYB holders earn fees in productive form (fees generate yield being a share of YieldBasis pools).

Fees collected and distributed after the Fee Switch activation (red line: the Bitcoin volatility index):

Sum: ~2.026 yb-cbBTC + ~0.719 yb-wBTC, totalling ~2.839 BTC (~$248k) accounting current redemption value. It’s important to highlight that tBTC didn’t earn any fees for veYB (poorly arbitraged & always imbalanced pool):

Lock-up stats & Governance

- 57.8m YB locked, resulting in 50.6m veYB; 71.37m YB are not locked

- 60% (~32.9m veYB) participate in voting for YB emissions distribution

- All governance proposals relating to protocol updates had a quorum of 57-61%, corresponding to the number of veYB holders who were active in YB emissions voting.

The opportunity to monetize veYB voting power via bribes was added on 30 October by Votium, but has not been used yet.

#3: Yield Basis influence on $crvUSD and Curve

Shortly before the launch of Yield Basis, there was a heated discussion in the Curve DAO regarding YB's influence on the crvUSD peg and stability. This discussion was repeatedly getting more attention during every credit line raise proposals.

Today, after months of Yield Basis operation it’s time to review the results:

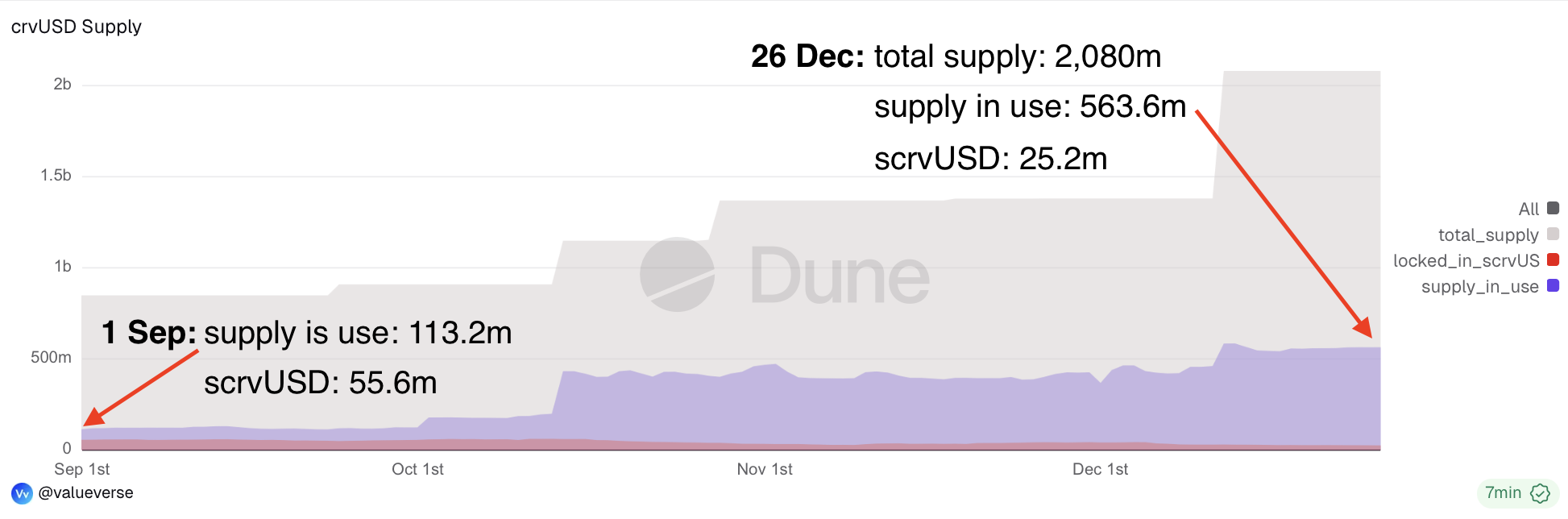

- $crvUSD supply: x5 growth (meaning actively used supply)

- $crvUSD weekly trading volumes: x5 growth

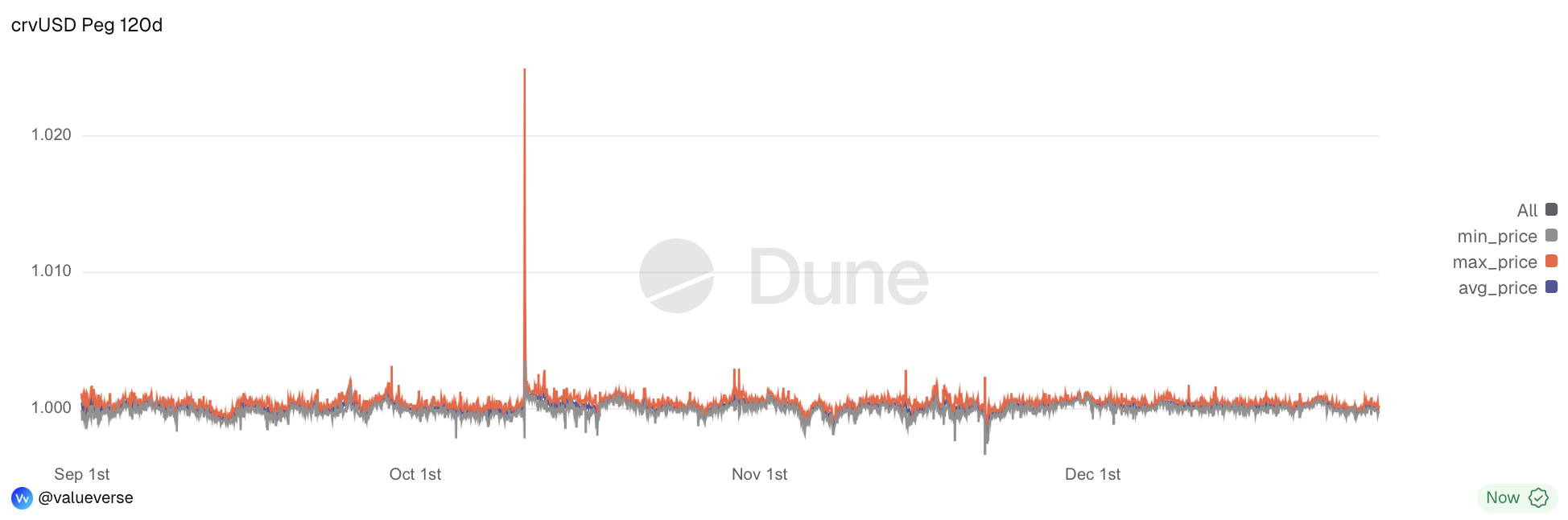

- $crvUSD peg stability: superior stability ($0.9966 minimal 120d price, $1.0001 average price)

The $crvUSD supply (total, in use, scrvUSD):

From 563.6m $crvUSD, 405.7m are in three Curve Cryptopools used by YB.

The $crvUSD peg before and after Yield Basis launch doesn't differ significantly (1.02 spike accounts for 10th of October):

Yield Basis provided 2.845m YB ($1.138m) for Curve $crvUSD stable pools bribes (as a Curve Licensing Fee) for $crvUSD liquidity.

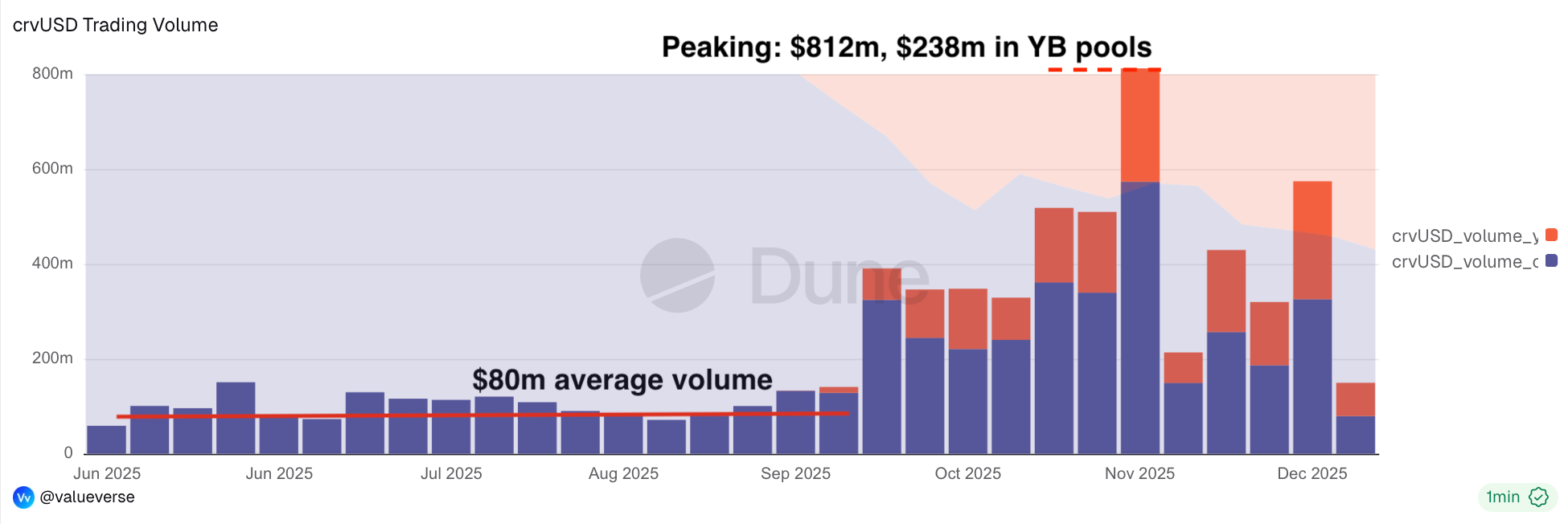

The weekly $crvUSD volumes covering all 38 active pools are presented below. Volumes in Yield Basis pools are highlighted in orange and a diagram showing the volume share of these pools is presented in the background:

Yield Basis operations account for a significant proportion of the overall $crvUSD volume, with a direct share of 46.8% (based on $crvUSD swaps in Yield Basis BTC pools only).

The overall weekly trading volume growth from ~$80m to an average of ~$410m (>5x growth) is a result of $crvUSD swaps in Yield Basis pools and following induced volumes in Curve $crvUSD stable pools & beyond.

Yield Basis 2026 Thesis

In 2025, Yield Basis proved that the brand new DeFi primitive — the leveraged AMM pool that eliminates impermanent loss — works and is economically efficient for liquidity providers (LPs) and the YB DAO that operates the protocol. It also clearly benefits the underlying infrastructure (Curve and $crvUSD), increasing adoption and generating additional revenue while preserving the peg.

#1 Yield Basis: the paradigm-changing solution for wrapped assets issuers

In our view, Yield Basis is more than just an IL-free AMM pool that offers yield with an improved risk-reward profile compared to ordinary AMMs.

Yield Basis is a superior product targeting wrapped native assets and tokenized RWAs issuers:

- Yield Basis pool theoretically could make any asset* productive (or enrich its productivity)

- Yield Basis pool establishes deep secondary market for an asset, allowing issuer not to spend on MM activities, but earn from it, simultaneously creating an yield option for asset holders

- The share of Yield Basis pools enables further Defi strategies for an asset in its new yield-bearing form (it can be used as collateral, etc)

*with sufficient trading volumes, volatility, and efficient arbitrage opportunities

It means that Yield Basis could act as a yield & liquidity infrastructure not only for wrapped BTC, ETH, BNB, SOL, and even ZEC, but also tokenized commodities such as Gold. It could also support highly traded and volatile tokenized stocks such as NVDA.

Following BTC, ETH, and other crypto assets support, we foresee YB-powered yield for Gold, Silver, and NVDA in 2026:

- none of these assets have significant onchain liquidity, and this is the result of Impermanent Loss in AMMs

- none of these assets earn yield (fun fact: NVDA pays 1 cent per $191 share in dividends)

- active usage of these assets is almost not possible by absence of liquidity & yield options (XAUT & PAXG biggest pools are less than $10m; lending options are limited due to absence of liquidation pathways)

Yield Basis could change everything not only for BTC yield, but also for markets of tokenized stocks & commodities, generating fees for LPs and YB DAO (veYB holders) from all these markets:

- Yield Basis offers a unique option to generate yield on assets that don't otherwise offer it, simultaneously ensuring secondary market liquidity

- Yield Basis could capture significant trading volumes and the subsequent fees.

- There also are other benefits, such as growing brand recognition by unique positioning, and additional revenue like bribes for veYB holders.

Tokenized Gold holders & traders wouldn’t choose another DEX: there will be no yield option on the market comparable to Yield Basis by APR & risk/reward profile, and no other deep liquidity source.

Only this would make Yield Basis the Defi cashflow machine of the cycle.

#2 YB utility expansion: priority access for veYB holders

Current YB token utility structure is based on a battle-tested vote-escrow model with an additional factor enhancing its intrinsic value - the mining cost.

However, YB is a core asset of a protocol with unique feature that never was present veToken-powered protocols - limited capacity to use the product:

- Yield Basis offers a product with a higher yield than any of its competitors', without the typical IL risk. This means providing liquidity has a risk/reward profile that isn't available otherwise.

- Every $1 of TVL earning yield in YB pools is limited resource

- At the moment, Yield Basis LPs have no barrier to entry since it works in the “first come, first served” paradigm.

If Yield Basis pools have such huge demand due to superior risk/reward properties (which is confirmed at every TVL Cap raise and constantly filled pools), it is logical to reserve some space exclusively for YB DAO members that actively participate in protocol operation & defining its future.

The veYB 2026 Thesis

- Reserve a share of the TVL cap in each $crvUSD-powered pool exclusively for veYB owners (according to the average veYB share per address over time)

- Allow veYB holders to delegate TVL allocation to any address with an option to set an yield_fee variable, which is a fee paid as a share of the LP's profit for using this delegated right to enter the pool.

- This new function will enable veYB holders to secure a guaranteed spot in YB pools, or generate yield by delegating this right to LPs who do not own veYB.

This will enable a new economic loop: veYB holders must govern the protocol to maximise TVL caps on those pools that are most efficient for protocol LPs (as well as the YB DAO):

- With maximised TVL caps on the most efficient pools, veYB holders will have the reserved capacity to provide greater liquidity to the best yield options themselves

- Another option will be to delegate this task to LPs in exchange for a share of their yield.

- As a result, the more efficient the pool is and greater is the yield, the higher is the percentage of profit that LPs will be willing to pay to enter the pool. It will form the yield market driven by organic demand to enter YB pools.

It also could lead to veYB accumulation by third-party DAOs and asset manager companies to have a guaranteed spot for their assets in YB pools, while the some share of the TVL could to be accessible on a "first come, first served" basis.