Cryptoeconomics 2026 Thesis

Introduction

The year 2025 was pivotal for crypto in terms of awareness, regulation, and adoption. At the same time, it was painful for holders and investors regarding pricing of assets, particularly altcoins. For newly-launched tokens, 84.7% are traded below their TGE valuation.

Crypto is ending this year with a significant divergence from the US stock market, which is trading near all-time highs due to Big Tech/AI growth and massive capital inflows anticipating interest rate cuts and liquidity expansion. At the same time, this new level of crypto adoption and market development has not yet been priced in.

It is the perfect time to explore the evolution of token design and valuation approaches, and what to expect in 2026 as the industry shifts toward fundamental value pricing. The Valueverse 2026 Thesis covers our value-focused observations, thoughts, and ideas regarding token design, yields, valuations, and related matters.

Important!

This is not a traditional report comprising hundreds of pages and covering every notable event in crypto. Instead, it offers a brief perspective from Valueverse token engineers and data analysts on cryptoeconomic design in 2025 and valuation approaches.

We do not aim to explore every token or protocol, as that is simply not possible.

Perhaps our perspective on certain matters will differ from that of other reports or X accounts. However, it is the plurality of opinions and the opportunity to view things from a different angle that truly drive in-depth understanding.

Bitcoin

Much has been said about Bitcoin developments and institutional adoption in 2025, as well as the future outlook for 2026. However, despite its global recognition as a store of value, the price remains below that of late January 2025 (the date of Trump's inauguration).

We propose that a possible explanation of what influences Bitcoin pricing—beyond general statements like “lack of liquidity & retail after Oct 10th”—could be one of the key Bitcoin-related learnings for this year.

Key reason: BTC OGs are monetizing their holdings by using BTC as collateral and selling call options. This triggers a sequence of market events that keeps BTC in a sideways trend and limits its growth.

The well-known Jeff Park delivered a quite detailed exploration of this point; we outline the key ideas and our observations here.

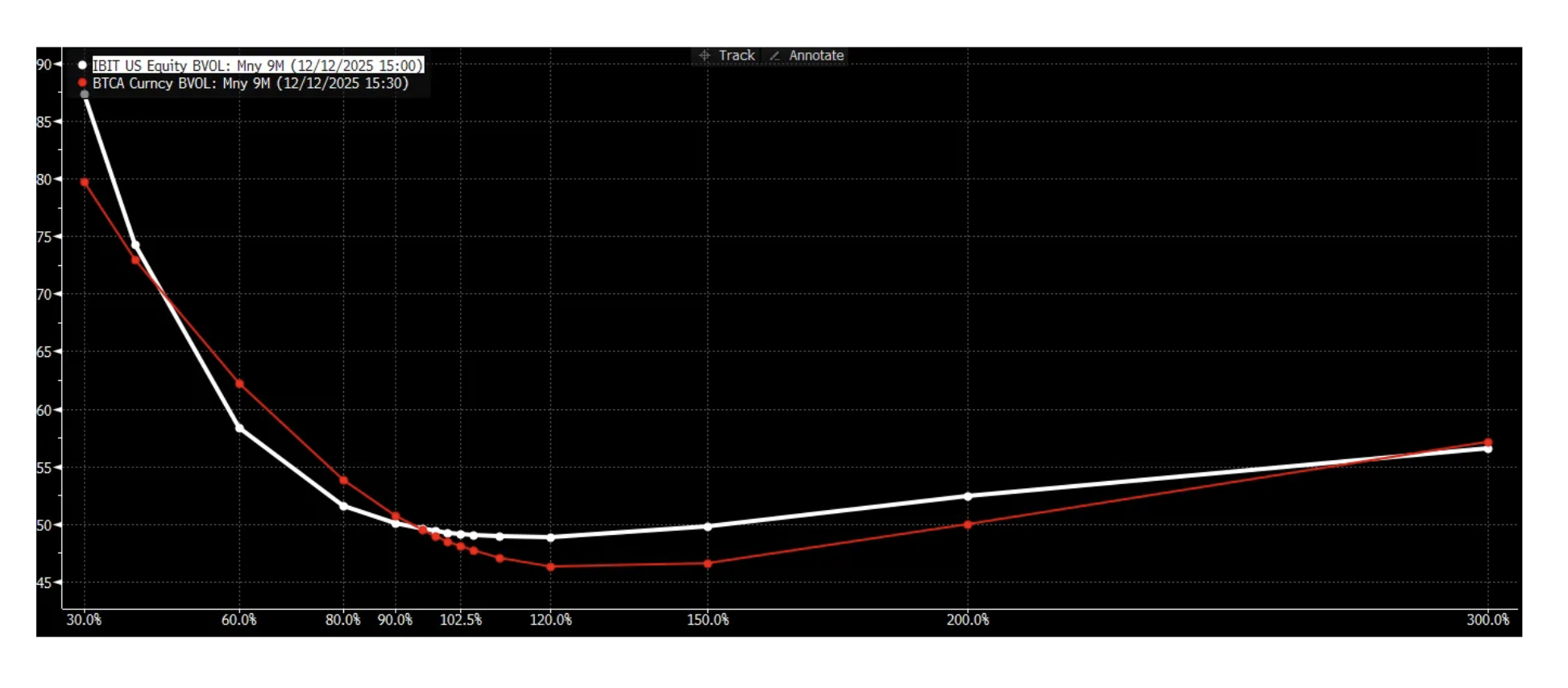

Jeff compares the implied volatility skew for IBIT (Bitcoin ETF) and native BTC options at Deribit:

https://dgt10011.substack.com/p/the-one-chart-that-explains-why-bitcoin

https://dgt10011.substack.com/p/the-one-chart-that-explains-why-bitcoin

IBIT has a positive call skew premium: this means that option buyers pay for upside strikes and expect growth. They buy upside volatility, creating upward pressure.

Native BTC options have a negative call skew (sloping through 150%): BTC holders sell upside volatility, creating downward pressure.

Consequently, IBIT buyers buy the ETF and sell call options, while BTC holders only sell calls since they already have collateral (they simply don’t need to buy anything). This adds negative delta to the market.

Step-by-step explanation of what happens: a large BTC holder sells a call option, which is automatically purchased by a Market Maker (MM). To manage the delta, the MM is forced to automatically sell BTC when the price rises and buy it when the price falls. As a result, when the price rises, BTC sales by Market Makers are quite large, restraining further price growth.

In 2026, Bitcoin will start to grow when (1) OGs stop selling calls (they will expect growth and stop selling calls to avoid limiting their profits on the upward move) or (2) IBIT and other ETFs dominate options flow, forcing market makers to hedge with the trend rather than against it. Last but not least—for this to happen, BTC growth requires significant volatility growth.

Takeaway: The market structure surrounding an asset could have a key influence on the pricing of its fundamental value.

Ethereum

In 2025, Ethereum implemented a massive lineup of upgrades focused on L2 efficiency, mainnet block gas limits, wallets (account abstraction), ETH stake size, and ZK cryptography, delivered with the Pectra and Fusaka upgrades.

Ethereum L1 is now incredibly cheap, with a sub-1 Gwei base fee, making L1 attractive for building mainnet dApps as user acquisition is no longer limited by gas fees. Consequently, L2 competition is now focused entirely on ecosystem value and products, rather than transaction price.

Following the Bitcoin DATs, Ethereum was under the institutional spotlight in 2025, with major buyers such as Bitmine accumulating around 5.6% of the supply.

However, the trickiest question widely observed this year has been how to value Ethereum.

Here we provide an overview of three approaches to this problem, proposed by William Mougayar (Independent Researcher & Founder of the Ethereum Market Research Center), Simon Kim (CEO, Hashed), and Konstantin Lomashuk with Artem Kotelskiy (Founder and Cryptoeconomist at Cyber.fund, respectively).

William Mougayar – Ethereum is a programmable coordination layer for the digital world. It is not a blockchain; it is a system with internet-like properties.

According to William, “Ethereum’s true economic power lies not in the fees it extracts (revenue), but in the vast ecosystem of value it enables (externalities). Traditional financial metrics fail to capture this ‘invisible’ infrastructure value.”

In the recently published original report, three main pillars for understanding the value behind Ethereum are proposed:

- Captured Value (Visible Equity): Accounts for the current market capitalization of native ETH and all other assets issued on Ethereum (L2s, stablecoins, DeFi assets) (estimated by William at $0.6–0.9 trillion).

- Economic Flow (Digital GDP): The value of all financial interactions & settlements powered by Ethereum (includes stablecoin flows, lending, swaps, RWA, and any other DeFi activities). William provides the assumption that the capitalized value of this “Digital GDP” ranges from 3 trillion.

- The Trust Surplus (Invisible Value): By design, Ethereum decreases so-called ‘transactional costs’ by removing unnecessary intermediaries for all types of economic activity and providing programmable trust. Transactional costs traditionally encompass expenses related to lawyers, insurance, and other costly measures that have no alternatives in the fiat economy, allowing economic agents to transact safely with one another.

William provides his estimate: “Analogous to the ‘consumer surplus’ generated by the Internet, this unpriced utility is valued at $150–600 billion.”

Regarding ETH as an asset, William focuses on its key role as a coordination tool for the Ethereum network. This allows the network to safely operate as a public good for world-scale settlements. This includes infrastructure reliability, incentivizing network participants, and cryptoeconomic security, creating and maintaining the aforementioned 'trust surplus'. Operational functions, such as using ETH to purchase blockspace (gas payments) and using ETH as pristine DeFi collateral, are considered technical functions surrounding the core coordination role.

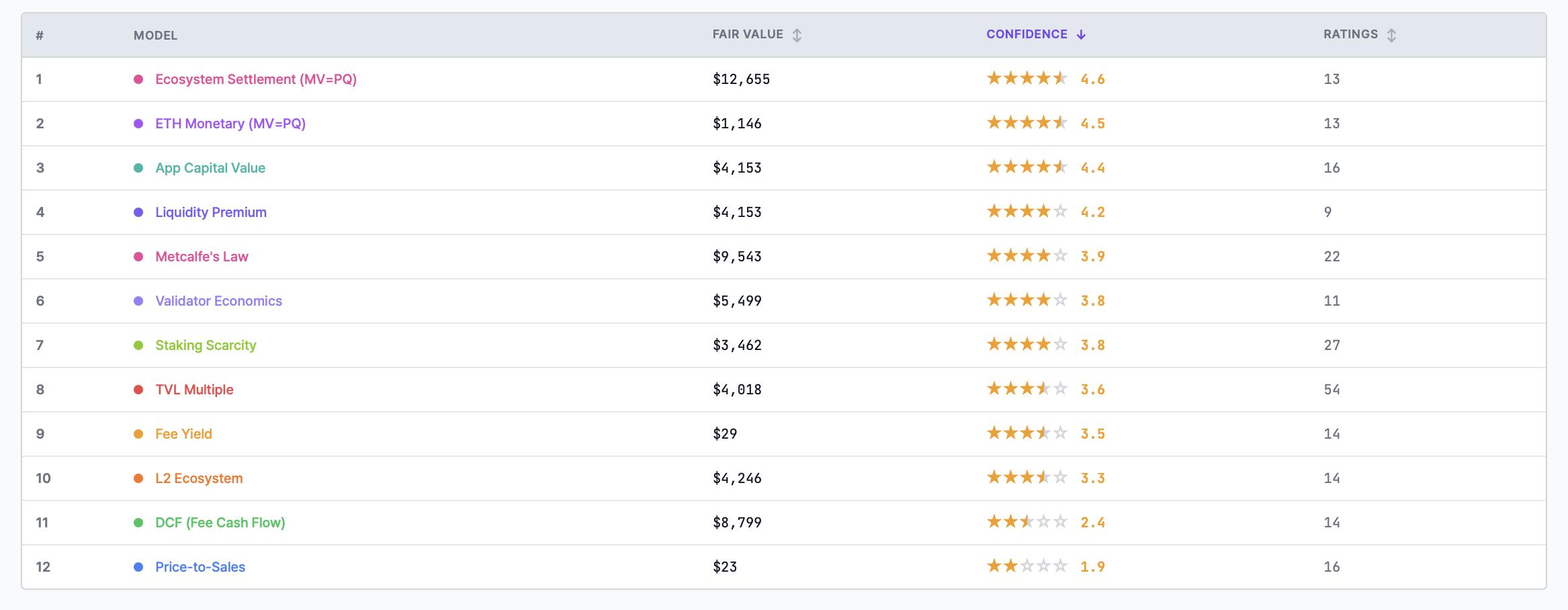

Simon Kim created ethval.com, a publicly accessible Ethereum valuation dashboard. The core idea is to use all possible valuation approaches to create a comprehensive picture from different angles via available data.

Ethval.com utilizes the 12 approaches presented below, which are ranked by community confidence:

The collective opinion demonstrates the following:

- The most confident metric is Ecosystem Settlement, valuing Ethereum as the settlement layer for the L1 and L2 ecosystem, including not only ETH but also stablecoins, token transfers, etc.

- The second metric values “ETH as money,” accounting for native ETH transfers only.

- The third metric values Ethereum as a programmable finance layer, considering the entire ecosystem value.

Staking Scarcity and Validator Economics, previously widely used to value ETH as a productive asset, are ranked only in the second half of the list.

The Cyber.fund’s report on Ethereum frames the network through a business strategy lens, making it more operational and product-oriented, with a focus on value capture mechanisms and the competitive blockspace market.

ETH's value is viewed as a foundational fuel and platform value accrual asset. The value accrual itself is discussed through specific network services (such as securing assets, economic flows, rollup operation, and data availability) and the related ETH revenue structure and growth possibilities. The report provides exceptional depth on the ecosystem structure, drawing conclusions based on on-chain data.

It is interesting that William Mougayar’s view on Ethereum and the results of Simon Kim’s valuations are generally aligned and focused on ecosystem value rather than valuing Ethereum as a revenue-based company (see Ecosystem Settlement & App Capital Value at ethval.com). The core difference is William’s Trust Surplus approach, which is extremely significant to consider as it represents the value of solving a historically existent economic problem known as “transactional costs”. The Cyber.Fund approach focuses more on the tangible business metrics of network operations, possible growth pathways, and ETH value accrual.

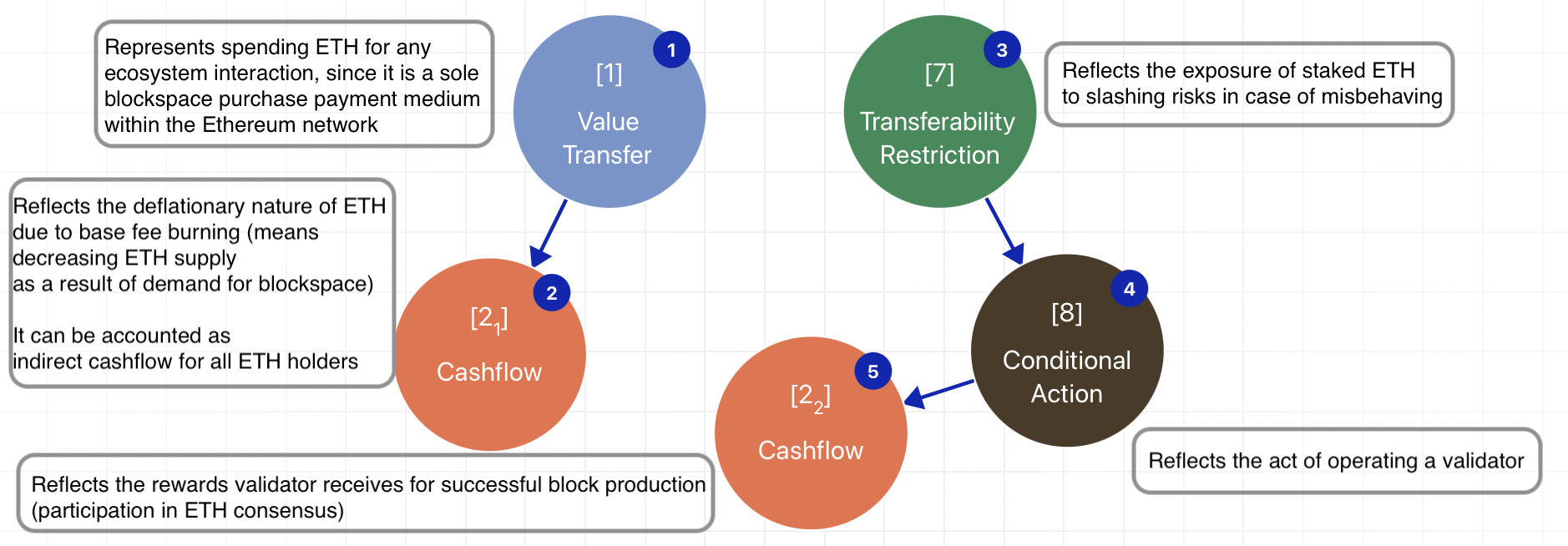

At Valueverse, we focused not exactly on valuing Ethereum, but rather on explaining the value-capturing structure of the ETH asset. For this purpose, we used the Value-Focused Token Classification framework, which accounts for Value Transfer and Consensus functions:

https://app.valueverse.ai/tokens/ethereum

https://app.valueverse.ai/tokens/ethereum

This aligns with the research discussed above:

- Value Transfer accounts for all value ultimately accrued by ETH from being used for any kind of state update (which includes any act of economic activity or settlement within the network), thereby triggering ETH deflation. Thus, the value of all Ethereum-wide settlements is accounted for in Value Transfer, while their influence on ETH supply is accounted for in the Cashflow component.

- Consensus accounts for validator activities resulting in cryptoeconomically securing Ethereum’s operation. This function consists of Transferability Restriction (reflecting that cryptoeconomic security is ensured by using ETH as a slashable security deposit, or what is known as 'skin-in-the-game,' by validators) and Conditional Action (the necessity to run a validator and honestly participate in block production), while Cashflow reflects the reward for successful consensus participation activities. The Consensus function explains the operation of Ethereum’s cryptoeconomic security layer, which specifically provides the Trust Surplus feature. A reliable and expensive-to-attack consensus mechanism is essential for network trust, as reflected by Ethereum's TVL and institutional adoption: money flows follow trust.

To conclude: we must acknowledge that Ethereum is one of the most complex assets to value in history, involving various approaches and perspectives.

While possessing easily measurable tangible value accruing to native asset holders and users, Ethereum also possesses significant “hidden value” that cannot be directly valued and whose valuation could be recognized by the market only at the order of magnitude scale of operation and adoption.

The revenue sharing trend

Reflecting on the ideas surrounding assets and their value, as well as the practical steps taken to change the utility of these assets (known as 'tokenomics updates' on X), it is evident that 2025 marked a turning point in the narrative around revenue and TradFi views on tokens.

The following major organizations highlighted this trend in their reports:

- Coinbase: "Governance-only" utility tokens will shift to "revenue-tied" models.

- Delphi Digital has observed a decline in the valuation premium for Layer 1 (L1) blockchains, as the market shifts focus towards "fat applications" and sustainable revenue models.

- Messari highlights that markets are now paying attention to protocol revenue and real economic activity, not just token supply/emission narratives.

Below is a list of token revenue pioneers who adopted this approach long before it became a huge trend:

- $BNB (2017, buyback & burn)

- $MKR (2017, burn via fees to repay the Single-Collateral DAI interest rate)

- $OKX (2019, buyback & burn)

- $CRV (2020, vote-escrow)

- $SUSHI (2020, using fees for buybacks and further distribution in SUSHI via the xSUSHI contract)

- $GMX (2021, fee distribution to stakers)

- $AERO (2023, ve(3,3) model).

However, it did not become mainstream until 2025, when market-leading protocols such as $UNI, $LIDO, $AAVE, and $HYPE upgraded their token design to include revenue sharing.

There are two principal approaches used for revenue sharing:

- Sharing application fees (or a dedicated part thereof) with token holders, conditioned on a specific action to distinguish those receiving revenue from those who do not. Technically, this is typically done by locking tokens in a special (often governance-related) contract that enables revenue-receiving eligibility.

Such an approach creates two token subclasses: a revenue-bearing version of the token and a version that is tradable but does not receive revenue.

- Using application fees to buy tokens from the market (commonly called ‘Buybacks’). This can be considered an unconditional revenue-sharing model where all token holders receive indirect revenue (which can be accounted for via the metric of supply reduction).

Some protocols use both of these simultaneously.

While the fee sharing option is easy to understand—since it provides token holders with directly accountable revenue in a way of "I hold 1 token complying with the lock-up/governance participation/staking condition and receive X USD over a period"—buybacks are trickier. The common criticisms of fee sharing include the possible taxation of this revenue in some jurisdictions and concerns related to the legal side of sharing revenue.

At the present moment, buybacks are used by some of the biggest protocols in the industry. The supporting theses are as follows:

- Regulatory Perspective: Buybacks are easier from a regulatory perspective since token holders do not directly receive any fees or monetary value. Some legal frameworks, such as DUNA, do not allow any direct fee sharing, making buybacks the only option for sharing value with token holders.

- Tax Efficiency: Buybacks are considered a tax-efficient value accrual option since they do not create a taxable event for the token holder.

- Price Support: Buybacks directly support the token price. Conversely, in the case of fee distribution, token price is supported by independent users who find value in buying and using the token to receive fees, based on the current token price versus the fee stream in a given period.

Criticisms of buybacks include:

-

Lack of Tangible Value: Buybacks do not provide tangible value for token holders other than possible price growth, which depends highly on other factors and market conditions.

Note: In the case of fee sharing, even if the token value declines, holders receive some additional value that they can use (distributed fee amounts, or revenue per token).

-

No Economic Loop: Buybacks do not enable any kind of economic loop, mechanics, or flywheel related to the token; they simply distribute value via an indirect mechanism.

Buybacks could support the price, but they don’t create coordinational value.

-

Lack of Utility: Buybacks are a form of financial engineering to fix the absence of real utility and demand for a token.

If you need a buyback to make a token valuable, why do you need the token at all?

-

Insider Conflicts: There is a conflict regarding insiders versus buybacks versus possible return-to-circulation. Who decides on the timing of the buyback (i.e., the token price) and the amounts? While the protocol buys back tokens, insiders could sell. If buybacks are not irreversibly burned, tokens could return to circulation, eliminating the core idea that supply decreases.

If buybacks are done algorithmically and burned, this problem is less significant.

Let’s observe examples of protocols that implemented one of these two models.

Notable protocols that implemented buybacks in 2025:

- Pump.fun $PUMP launched buybacks (without burn) and is trading around All-Time Low (ATL) levels, despite spending 1.24 million $SOL (~$221m accounting for the $SOL price at each buyback event)

- World Liberty Finance $WLFI implemented buybacks and burned $36m of $WLFI-denominated fees.

- Hyperliquid $HYPE spent $684m on buybacks. Total expected unlocks are much larger than what the current annualized protocol revenue could buy back.

- AAVE $AAVE spent $30m on buybacks, with a proposal to spend $50m annually.

There are fewer examples of direct fee share implementations in 2025, and all of them utilize the vote-escrowed token model:

- Yield Basis $YB, a protocol that solves impermanent loss in AMMs (created by Michael Egorov, the inventor of the veTokenomics model).

- Momentum Finance $MMT, a ve(3,3) model DEX on Sui

Other notable protocols launched in 2025 using variations of the ve tokenomics model that do not have a direct fee-sharing feature are $VIRTUAL and $ALMANAK.

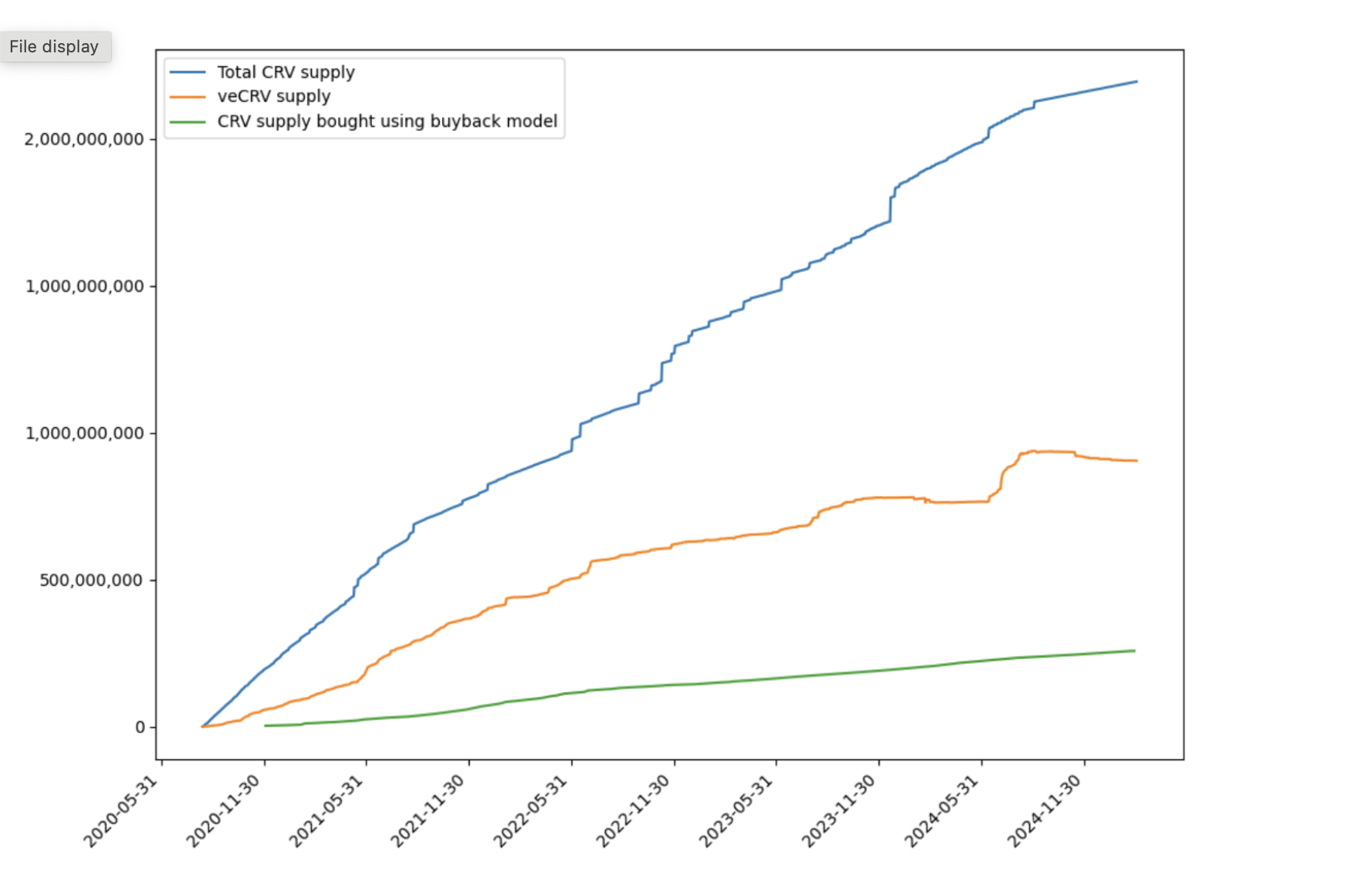

Thus, we can conclude that the tokenomics narrative is clearly dominated by the buyback idea. In this context, it is worth mentioning Curve’s report, “A Comparative Analysis of VE-Model and Buyback Model for DeFi Tokenomics: Curve.fi example.”

It proves the efficiency of veTokenomics over buybacks for $CRV. Our conclusion is as follows:

Using long-term lock-ups and direct fee sharing, it is possible to reduce token supply by locking them almost forever for a fraction of the cost (provided as fees) compared to direct buybacks.

Here is our own theoretical example of how switching $HYPE from a buyback-only model to a buyback + fee sharing model could positively affect Hyperliquid.

Aerodrome $AERO is an example of using a combination of buybacks and fee sharing. The project implemented buybacks via the Public Goods Fund & Flight School and spent $33.8m on $AERO purchases. At the same time, $AERO has a fee sharing mechanism in its veTokenomics that generated ~$192m in value for veAERO holders ($AERO rebase income is excluded from this number).

To conclude this section: revenue sharing is a well-established trend that currently uses buybacks as the mainstream revenue distribution mechanism. As token engineers, we believe that direct fee sharing is more efficient and valuable for token holders. We foresee much wider adoption of it in the future.

Notable Achievements in 2025 (Non-Mainstream Edition)

Many achievements across market sectors and projects were widely discussed on X and in reports.

Here, we highlight several achievements that, in our opinion, are truly huge and deserve much more attention:

Yield Basis Solved Impermanent Loss Since the invention of AMMs, the problem of Impermanent Loss was a major issue that no one could truly solve. That was until 2025, when Yield Basis finally solved it by launching a live product with $200m in TVL and profitability (up to 28% BTC yield) via its IL-free leveraged AMM pools.

We followed Yield Basis closely from day one, publishing a first-ever report explaining the protocol in detail. Recently, we delivered the Yield Basis 2026 Thesis, foreseeing the application of IL-free pools to the massive market of tokenized gold and stocks.

One of the Few Decentralized Stablecoins Has Gained Significant Adoption

The $crvUSD (Curve’s native stablecoin), one of the few truly decentralized stablecoins, has significantly expanded its market share. Here is why it truly deserves to be a notable 2025 achievement:

- It surpassed $GHO (Aave’s native stablecoin) in supply ($563m in circulation vs. $495m).

- ranked #3 in total stablecoin volumes (during high volatility), right after $USDT and $USDC.

It is worth mentioning that this happened after the launch of Yield Basis, which utilizes $crvUSD for IL-free Bitcoin pools.

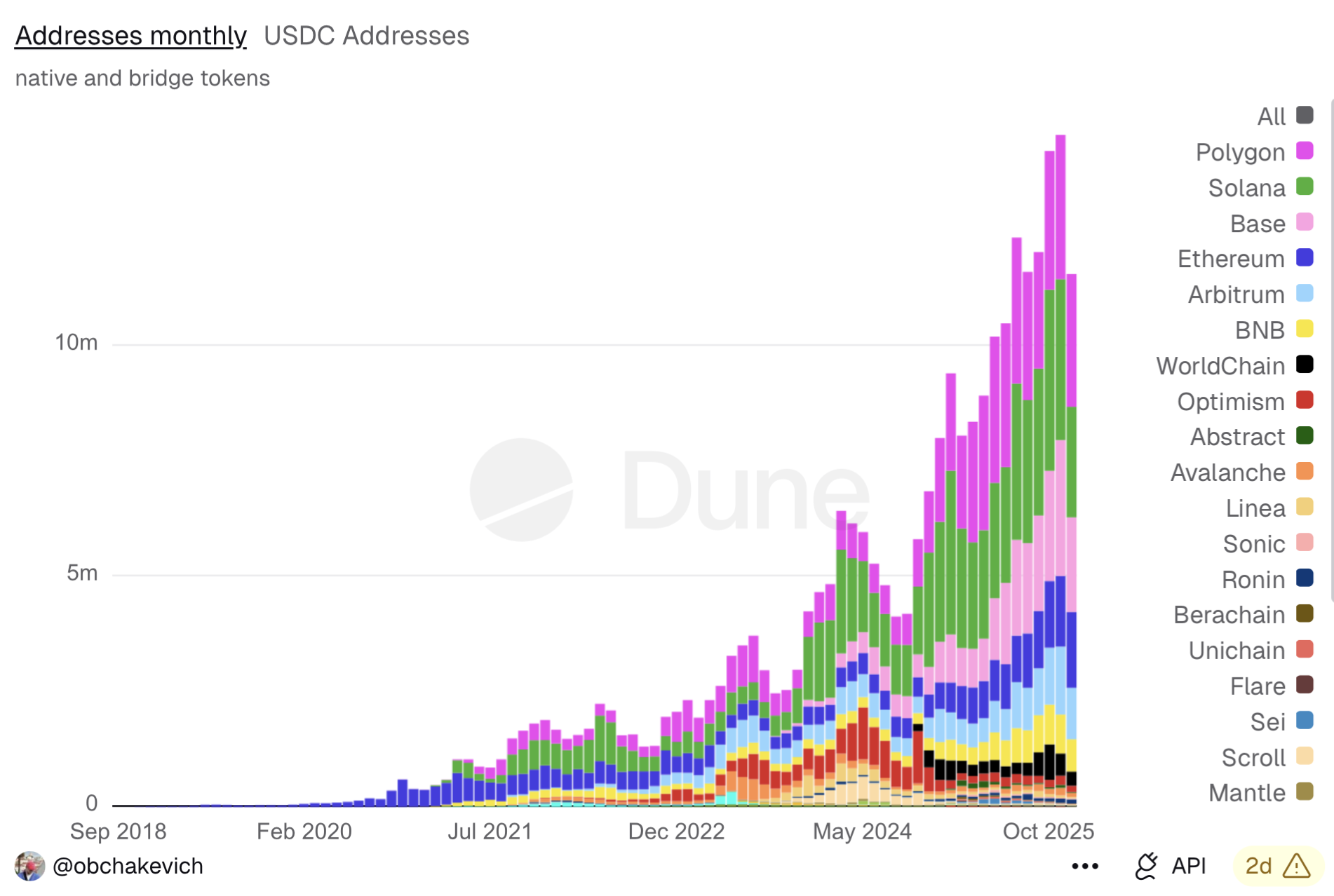

Polygon Gained Significant Traction as a Stablecoin-Focused Chain

This year, the stablecoin narrative reached a new level with the emergence of several major platforms (such as Plasma, Stripe, and Tempo) designed specifically to facilitate stablecoin payments.

However, Polygon is a project that has existed for years and has gained significant traction in stablecoin transactions. Some time ago, the chain shifted its focus to stablecoin payments and settlements, and these are the results.

Polygon leads in new addresses using $USDC, showing huge growth this year:

https://dune.com/obchakevich/polygon-pos-payments

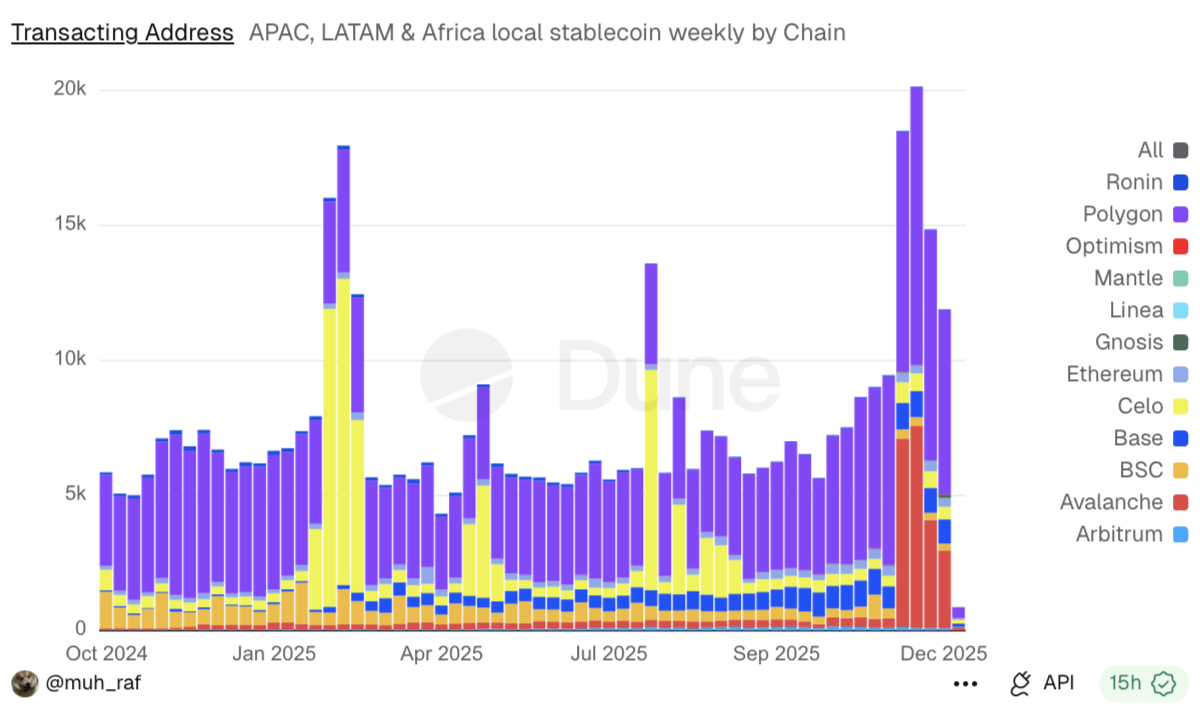

Polygon dominates in active user addresses transacting with local stablecoins in APAC, LATAM, and Africa.

Furthermore, Polygon is the home of Polymarket, the leading prediction markets application. It also develops its own ZK interoperability solution, Agglayer, which allows users to transfer huge amounts—like thousands of ETH—in seconds, preserving all fees within the Polygon ecosystem.

Financial results follow the clear focus on the stablecoin business:

- Polygon PoS maintains stable ecosystem metrics that hold up well even during depressed market periods, as it does not rely on traditional crypto use cases.

- The ecosystem ranks in the top 10 by TVL ($1.2 billion), TPS (50-80), and stablecoin market cap ($3 billion).

- The chain generated $6m this year in transaction fees (for comparison, Plasma generated only $6.7k in December).

Our impression after studying this data (thanks to one of Polygon’s advocates, Vadim) is that Polygon is very close to being fully established as an Ethereum payment layer.

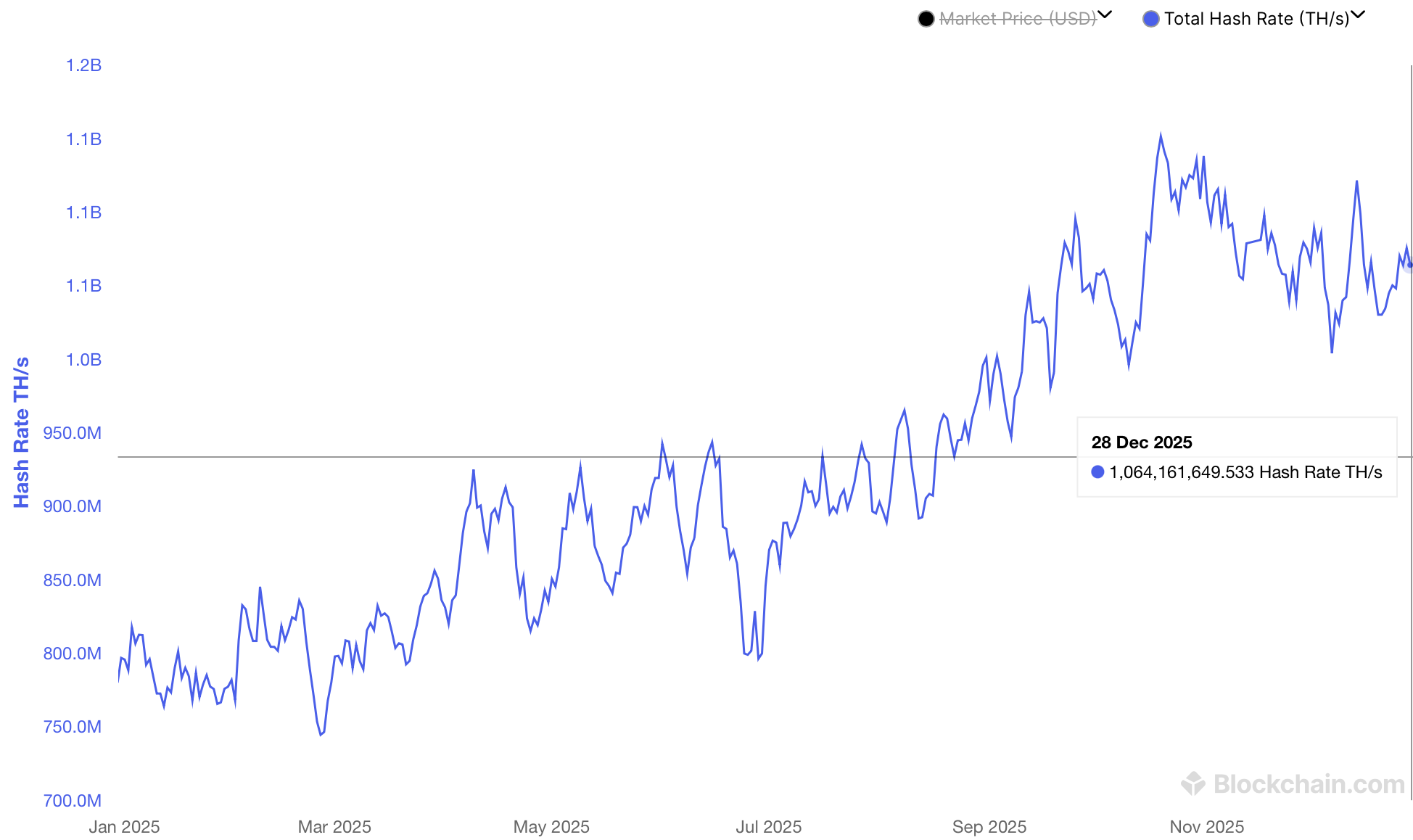

Tokenized Bitcoin Hashrate as a Successful RWA Asset

The RWA narrative in 2025 was huge. However, there is one RWA asset that gained significant adoption but is completely overlooked: Bitcoin hashrate.

GoMining pioneered this idea in 2023 and gained significant traction that well deserves a spot in this report.

It is interesting because tokenized Bitcoin hashrate is one of the rarest forms of real-world assets (RWA) that pay yield in crypto. It pays yield derived from Bitcoin mining in the form of native Bitcoin, minus costs related to electricity and maintenance. These costs can be decreased by using $GOMINING, which combines a discount and veTokenomics.

So, what are the specific results of Bitcoin hashrate tokenization? GoMining tokenized more than 1% of the total Bitcoin hashrate (precisely 1.138%), which is used by 4.8 million users:

The overall Bitcoin hashrate chart is presented below:

https://www.blockchain.com/explorer/charts/hash-rate

YOYO Tokenomics model

It is quite rare when a completely new form of economic design enters the market. The YOYO model is such an example.

Originally, it was invented and deployed by TokenWorks for accumulating and re-selling blue-chip NFTs such as Crypto Punks, Pudgy Penguins, and others.

How it works:

- An ERC-20 strategy-specific token is deployed at an initial valuation and is freely tradable upon deployment.

- All token purchases occur in a special pool that charges a fee on every swap, and this fee goes to a temporary holding contract.

- When the amount of accumulated fees reaches the price of the cheapest NFT offer, it automatically purchases the NFT.

- When the NFT price reaches a certain profit level, the NFT is sold and the profits are used for buying back and burning the strategy-specific token.

However, this model only works well in a growing market. If the NFT floor price drops below the purchase price, no NFTs can be sold for a profit. Consequently, there are no buybacks, and the fundamental token value decreases significantly until the market enters a growth phase (since buybacks and burns are the only value drivers for the token).

However, this model becomes much more resilient to market cycles when applied to the accumulation of NFTs with cash flow.

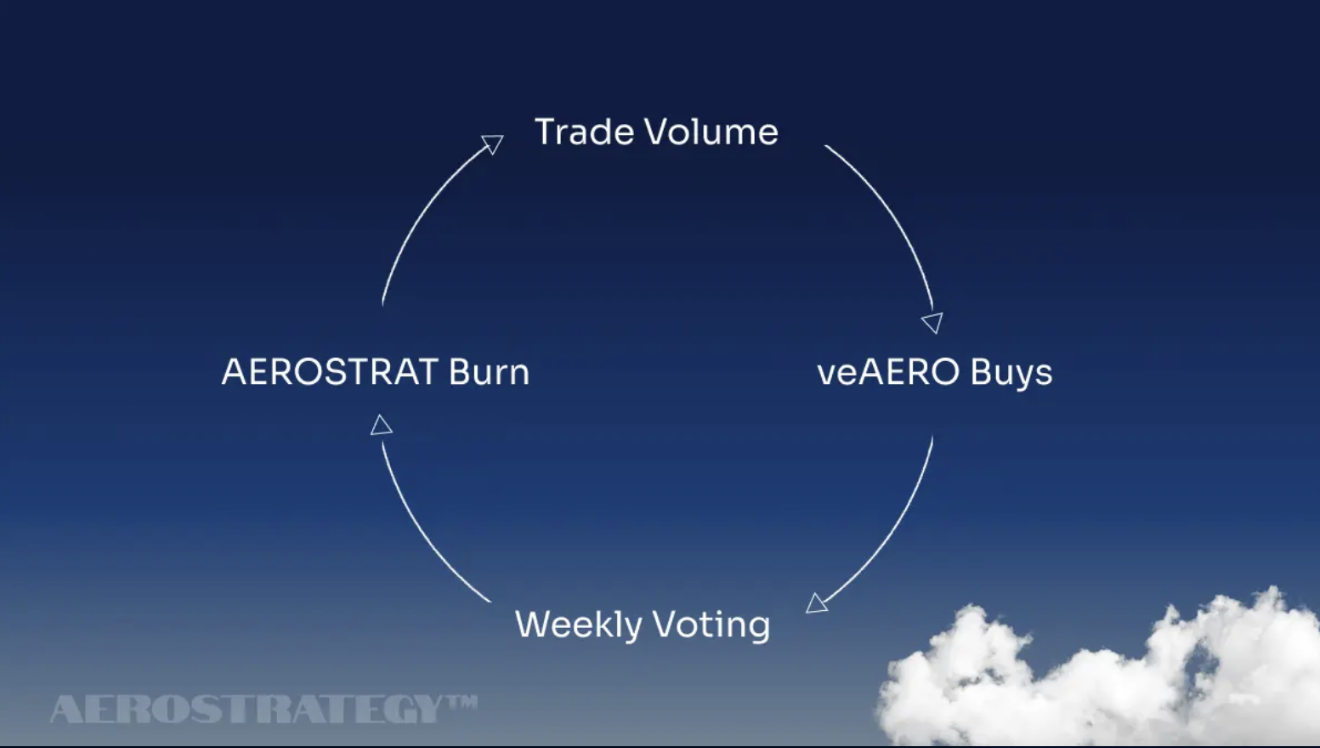

Aerostrategy pioneered this idea, developing a protocol that accumulates veAERO using the YOYO model. How it works:

- When users buy or sell $AEROSTRAT using the $AERO token in a specifically designed Aerodrome pool, they pay a 10% tax.

- Eighty percent (or 8% of the swap) is used to accumulate veAERO NFTs at the maximum possible discount on the secondary market.

- veAERO voting rights are delegated to autopilot.xyz and generate yield that is used for buying back and burning $AEROSTRAT.

Accumulating an asset with cash flow creates a self-sustaining model:

- If $AEROSTRAT has significant trading volumes (regardless of whether the market is actively buying and the token is growing, or holders are selling and the market is declining), veAERO holdings grow rapidly.

- If the market is down (as is the case today) and trading volumes are low, and the token price is relatively low, the veAERO yield slowly but surely buys back cheap tokens and removes them from circulation, appreciating its value.

What is a more traditional finance (TradFi) analogy for such a design? If you buy a token, you become a member of the yield vehicle and hold its shares (in the economic sense). However, you need to pay an entry fee, which is used to form the yield vehicle's capital. This capital (veAERO) generates yield originating from fees captured by the Aerodrome ve(3,3) tokenomics model.

We expect to see more applications using this approach in the future.

Cryptoeconomics in 2026

By 2026, we expect the industry to shift even further toward a narrative of revenue and overall fundamental token value. This is a clear trend, which is why we are working on Valueverse—a tool for understanding, tracking, and analyzing token value at scale.

Institutions measure value in two ways: infrastructure (network effects and high growth potential) and revenue (applicable to DeFi products and applications).

Our vision on the future of the revenue trend:

- Paradigm shift from generic metric of Mcap/revenue(FDV/revenue) to

Value of claim-bearing token supply divided to Revenue actually accruing to those tokens. We named it Mcap(VR) or Value-Receiving Mcap; alternative naming is Efficient Market Cap - Revenue sharing in form of buybacks or direct fee sharing will become much more adopted than in 2025

- It will be important to no analyze current state of revenue and efficient M.Cap relations, but also build a live prediction models taking into account that protocols are quite transparent systems, and the only step to get it done is to have a deep understanding how everything works and process the data fast (we’re working on it)

Our vision for the future of token design & analytics:

- The importance of building institutional reliability, foundational research, and monitoring token health cannot be overstated.

- Tokenomics terminology must interface with TradFi concepts, and explanations must withstand regulatory scrutiny.

- Tokenomics models will be judged based on value sustainability (or revenue sustainability). Novel design is not the only path to success.

- Token analysis must demonstrate the interdependencies of mechanisms. Metrics alone are insufficient without the context of value flows.

- Narratives based on fundamentals are more important than the noise from CT KOLs, as CT doesn't matter for retail.

- Comparative analysis is as important as analysis in isolation. It reveals relative strength, value captured per unit of risk, and mechanism efficiency when comparing similar tokens.

In closing, none of this can be done manually. To scale token analytics in 2026, we need to apply AI and automated data analysis.

Disclaimer:

This document is provided solely for informational and educational purposes and does not constitute, and should not be construed as, investment advice, financial advice, legal advice, or any offer, solicitation, or recommendation to acquire, dispose of, or transact in any digital asset or financial instrument. The information contained herein is based on sources believed to be reliable but is provided “as is” without any representation or warranty of any kind. Digital assets involve substantial risk, and past performance is not indicative of future results. Readers are solely responsible for conducting their own due diligence and seeking independent professional advice prior to making any investment or financial decisions.