Mid-Q1: A State of Yield Basis

The recent market volatility showcased Yield Basis capacity as a key onchain liquidity source for wrapped BTCs at Ethereum (see our previous YB 2026 Thesis report).

We tracked protocol operations in detail and provide this report covering the most important stats & observations:

- Protocol Performance (trading volumes, fees, veYB income)

- Yield Basis future trajectory explanation (proposed updates)

Key Stats TL;DR

- $BTC APY since pools inception ~26% (70% APY during 19 days of volatility)

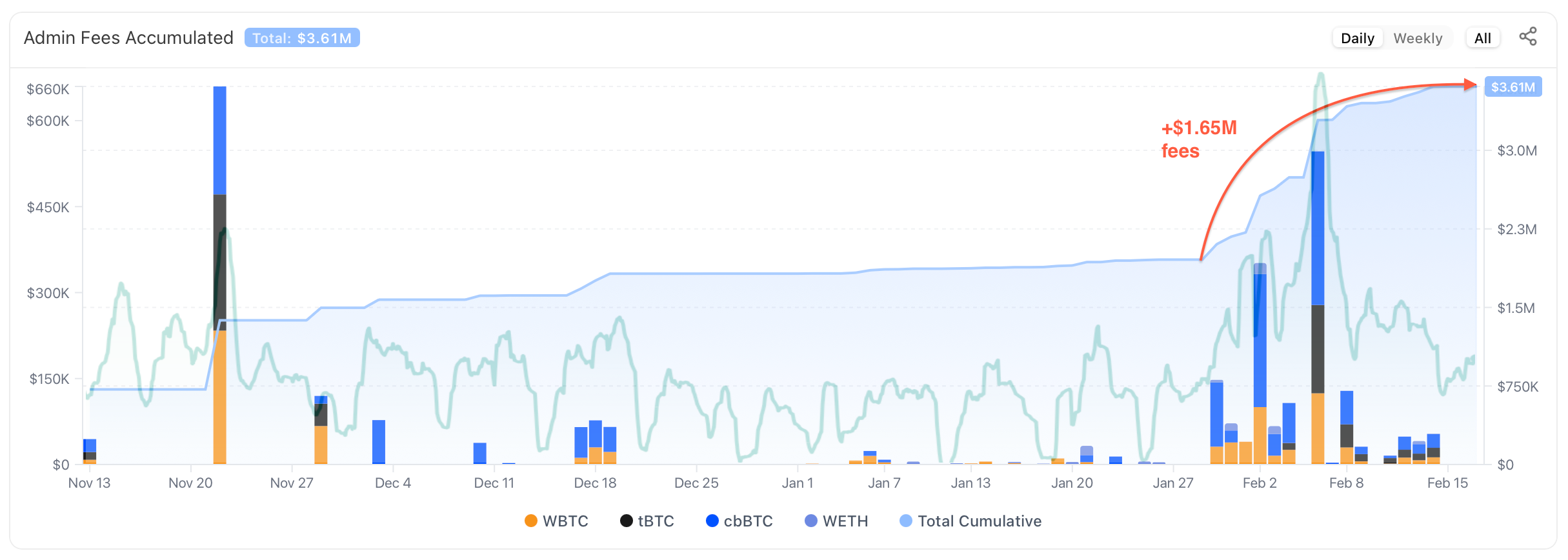

- During recent volatility protocol generated $1.65M of protocol fees

- Protocol is net profitable (earned +$6.84M LP+veYB fees vs. emissions cost since v2 pools launch)

We begin with an updated conceptual framework outlining how Yield Basis operates.

Yield Basis: Conceptual Overview

Yield Basis represents a structured product that tokenizes a dynamically rebalanced, gamma-neutral leveraged LP strategy, rather than a standalone AMM design as it is frequently interpreted.

Depositing $BTC to Yield Basis, the user receives $ybBTC that must be considered as a tokenized share in the IL-elimination strategy.

Table 1. Comparison of Basic AMM design vs. Yield Basis LP position design.

| Features | Basic AMM | Yield Basis |

|---|---|---|

| Simple explanation | Sells winners, buys losers following in any market direction | Keeps winner inside LP position: Adds more winners during growth (adding debt) Decreases position size during downtrend (reducing debt) |

| Risk Sensitives/Greeks Value Sensitivity Surface | Delta: ~0.5 Gamma: Negative Convexity: Negative | Delta: ~1 Gamma: Neutral Convexity: Positive |

Strategy basics:

- User deposits 1 wrapped $BTC to Yield Basis

- Protocol takes a 100k $crvUSD loan for that, forming 1 $BTC - 100k $crvUSD position in Curve Pool. This is the point where a 2x leveraged position is created.

- Further, protocol automatically maintains 2x leverage updating it if $BTC price grows or declines (see below).

A dedicated contract - LEVAMM serves as the $crvUSD minting market and holds both unutilized (allocated but not deployed) $crvUSD and Curve LP tokens (minted at position inception).

$ybBTC holders effectively own a pro-rata share of this contract, which corresponds to the underlying $BTC exposure that can be redeemed from the LP positions.

LEVAMM operates as a dynamic leverage rebalancing mechanism:

- In rising BTC markets: as $BTC price increases, DTV falls below the 50% target, triggering additional borrowing of $crvUSD and deployment into LP positions (minting new LP tokens)

- In declining BTC markets: as $BTC price decreases, DTV rises above the 50% threshold, triggering debt repayment and LP unwinding (burning LP tokens)

If $BTC grows, it means the amount of $BTC owned by YB LPs ($ybBTC holders) decreases, so protocol adds new LP tokens (by motivating arbitrageurs to do that) and restores the amount of $BTC owned by $ybBTC.

We created a Visual Explainer for re-leveraging mechanism that explores this process step-by-step according to the real contracts logic.

Protocol Performance summary

General Performance Metrics

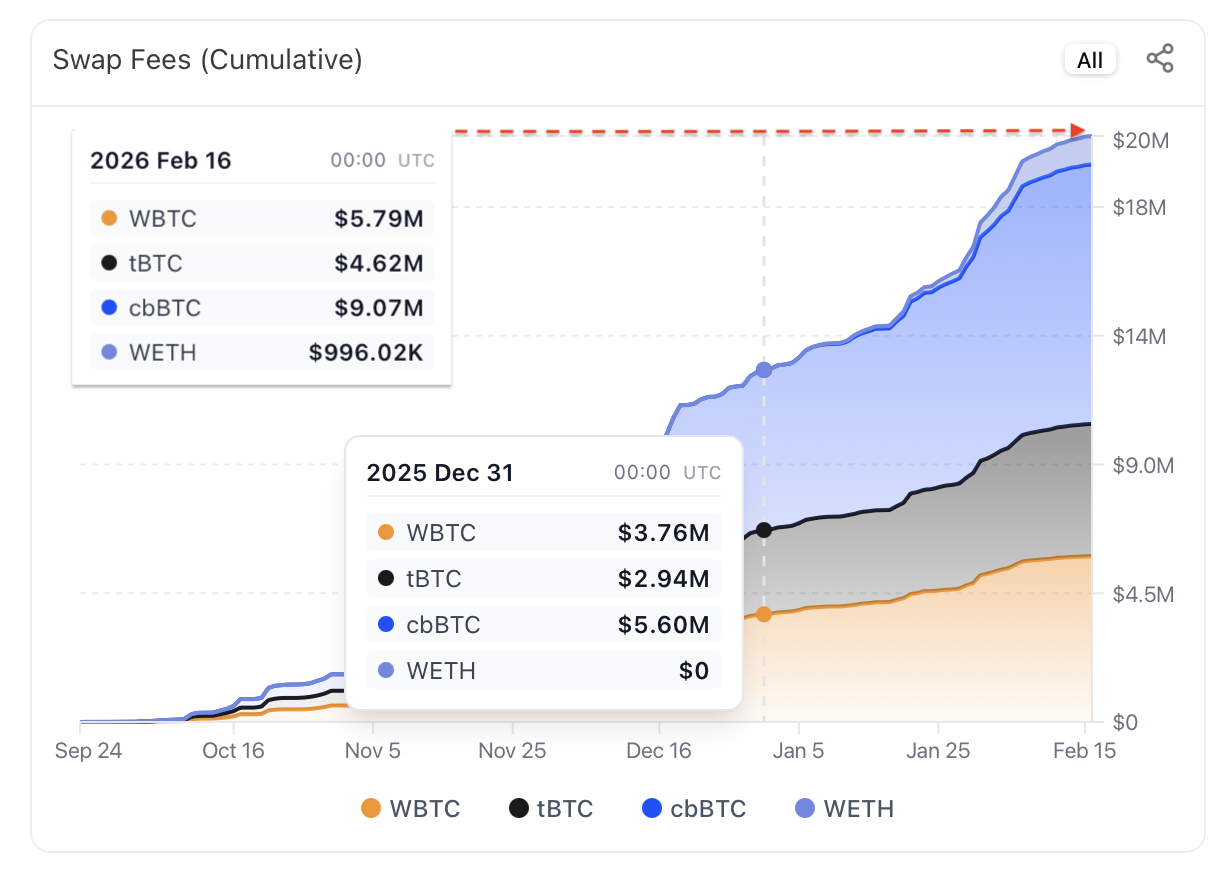

Starting from 1st Jan 2026, Yield Basis pools processed ~$769M trading volumes, resulted in $8.17M swap fees in Curve-hosted cryptopools:

The major share of trading volumes and fees ($436M volume, 57% swap fees) was captured since 28 Jan when the sharp $BTC downtrend started.

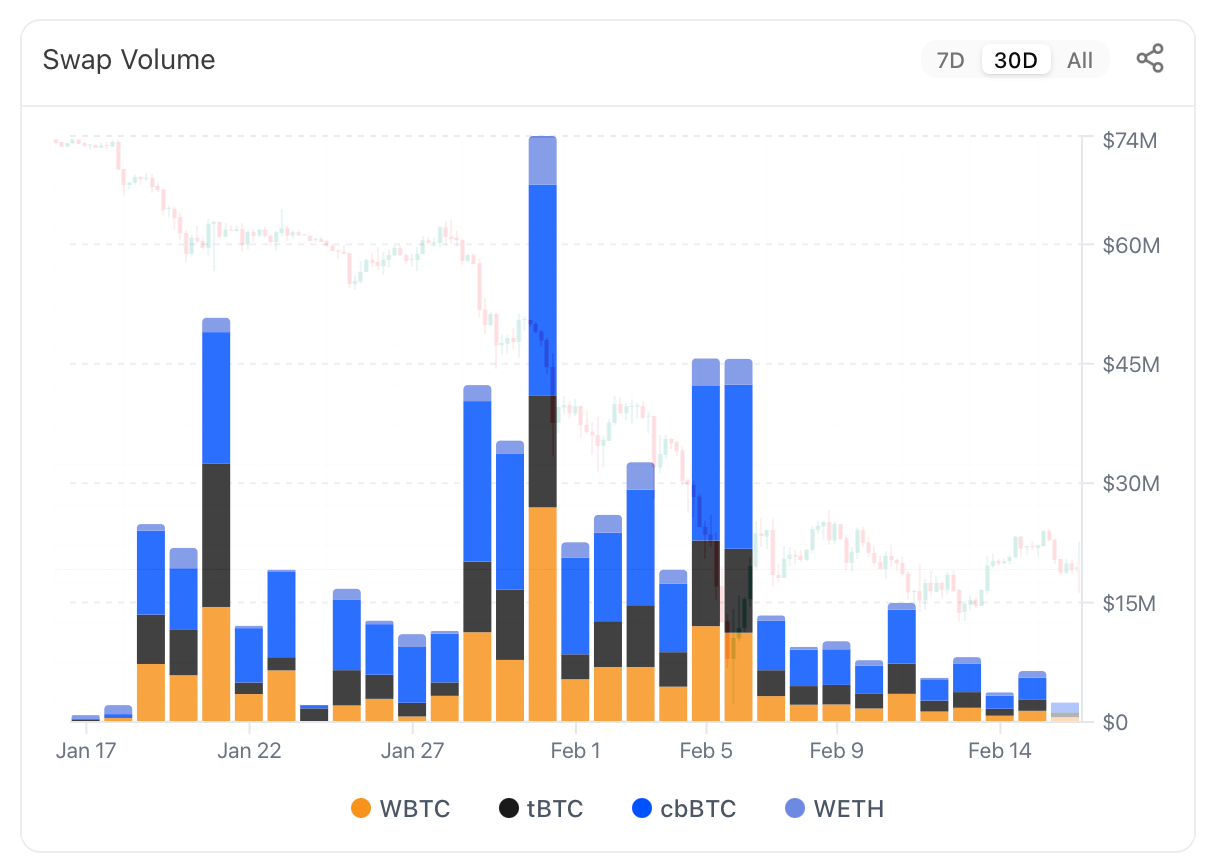

The most trading volumes were captured during $BTC price drops and following short-term recoverings:

Note, that captured fees ≠ income of LPs and token holders since it is partly used for pools rebalancing and maintaining 2x leverage necessary for eliminating Impermanent Loss.

Liquidity Providers Stats

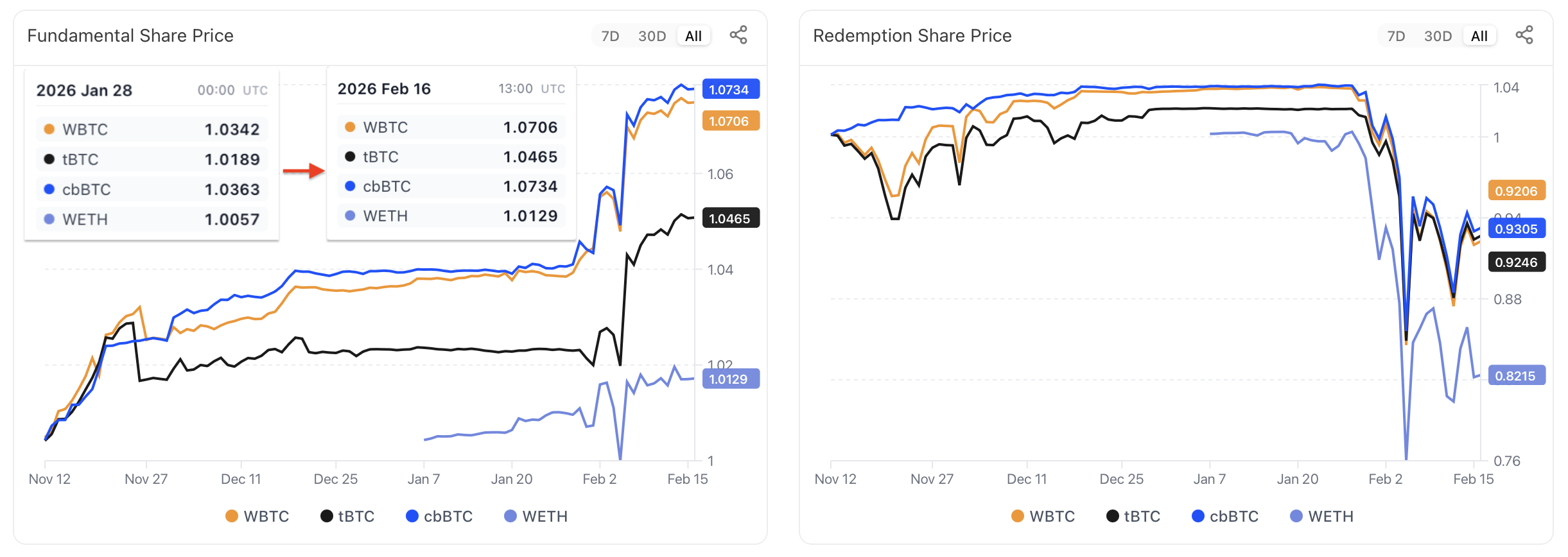

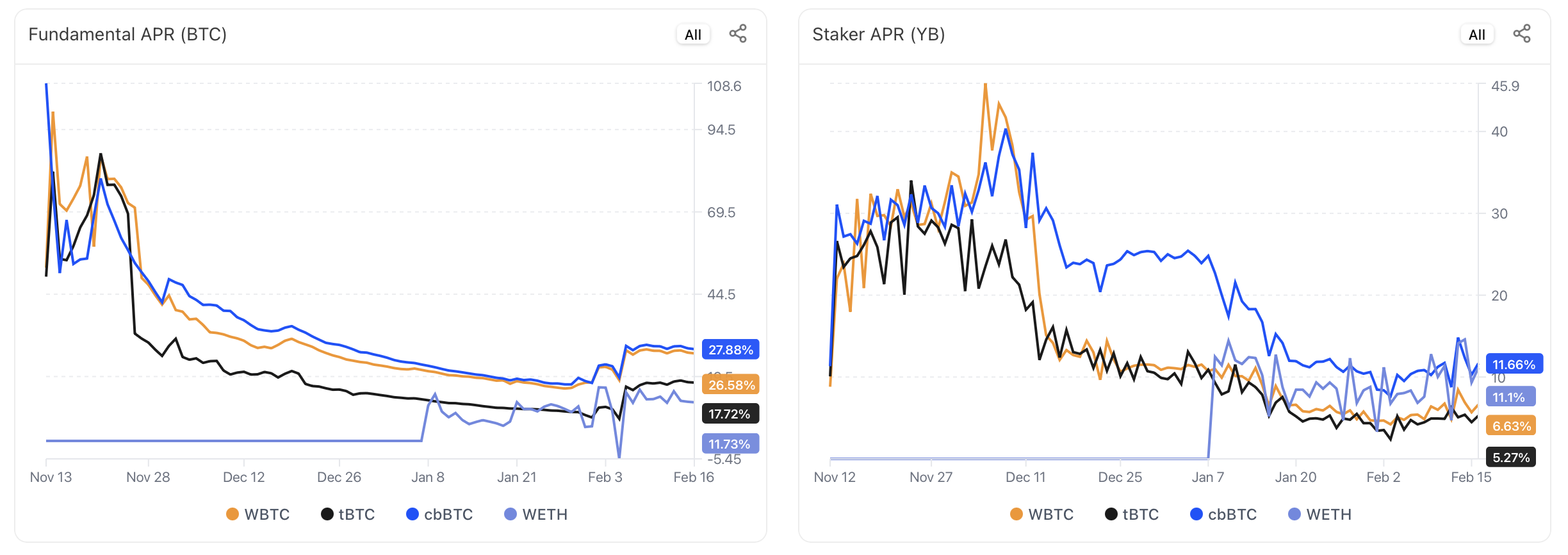

Since 28 Jan, LPs earned ~70% APY in $BTC during 19 days of volatility (counted by fundamental PPS):

Organic APY for Yield Basis LPs, measured via fundamental PPS growth since pool inception (12 Nov 2025), stands at ~26–27% for $cbBTC/$wBTC pools and ~11% for $WETH pools.

In contrast, staker APR (denominated in $YB emissions) has declined significantly, primarily driven by the decrease in $YB token price.

However, fundamental price per share is only one metric reflecting the value of LP positions. The Redemption PPS significantly declined, reflecting disbalance in Curve Cryptopools:

These disbalances are reflected in TRD (Temporary Redemption Discount) value meaning LPs which exit positions withdrawing exact amounts of assets according to fundamental PPS.

The Fundamental vs. Redemption LP value (TRD) needs additional explanation since it is commonly misunderstood. A good review on this topic is available here.

YB revenue & emissions analysis

Yield Basis captures substantial yields from volatility both for LPs and token holders.

During the recent $BTC volatility, protocol generated $1.65m for veYB holders (or ~46% of total veYB fees captured):

Protocol fees are captured in $BTC and $ETH YB LP tokens so this amount reflects ~$70k $BTC/$2k $ETH price and -13% TRD. It means that these amounts can be much bigger depending on pools' balance and $BTC/$ETH prices.

As a result, $YB revenue multiplier (price of the future revenue, calculated using average token holders' revenue during the entire protocol operation, not just recent weeks) dropped to ~1x.

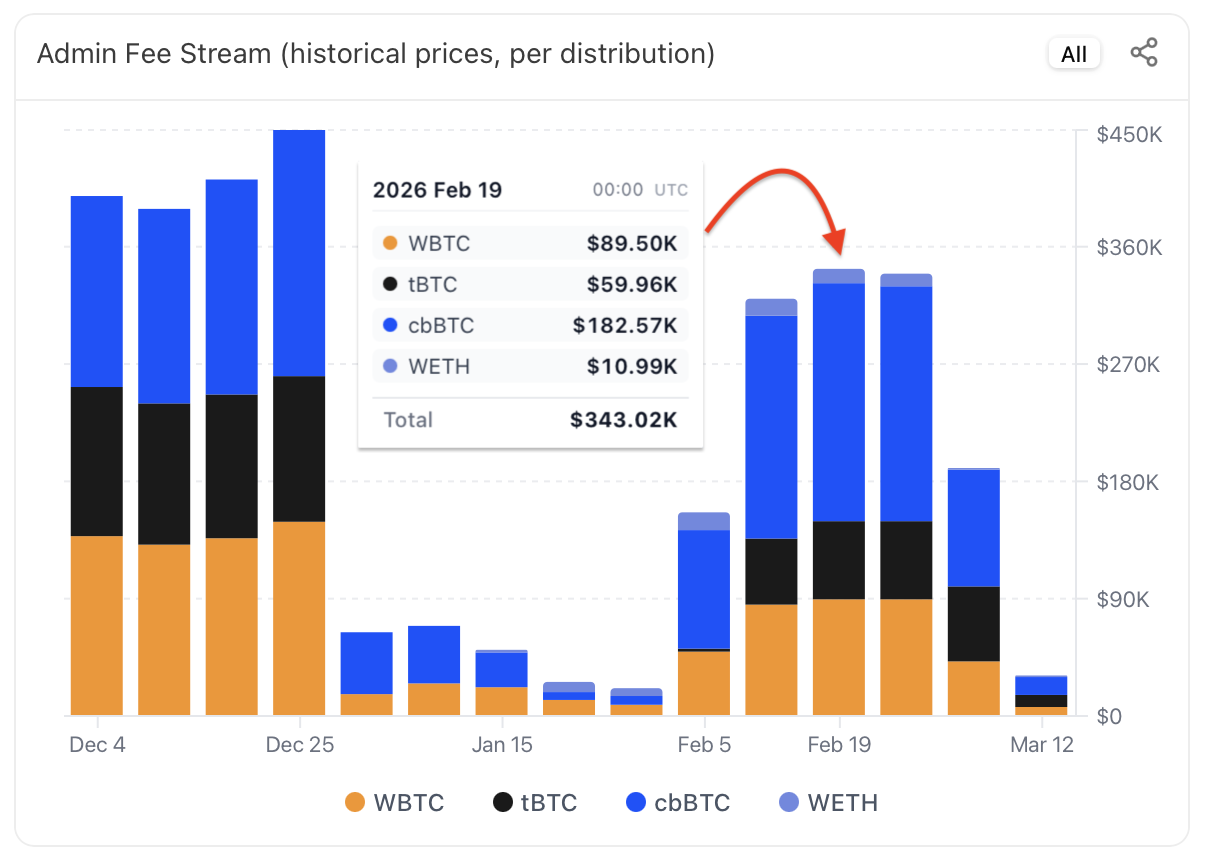

All captured fees will be claimed over four weeks, so weekly APY has ~150% benchmark:

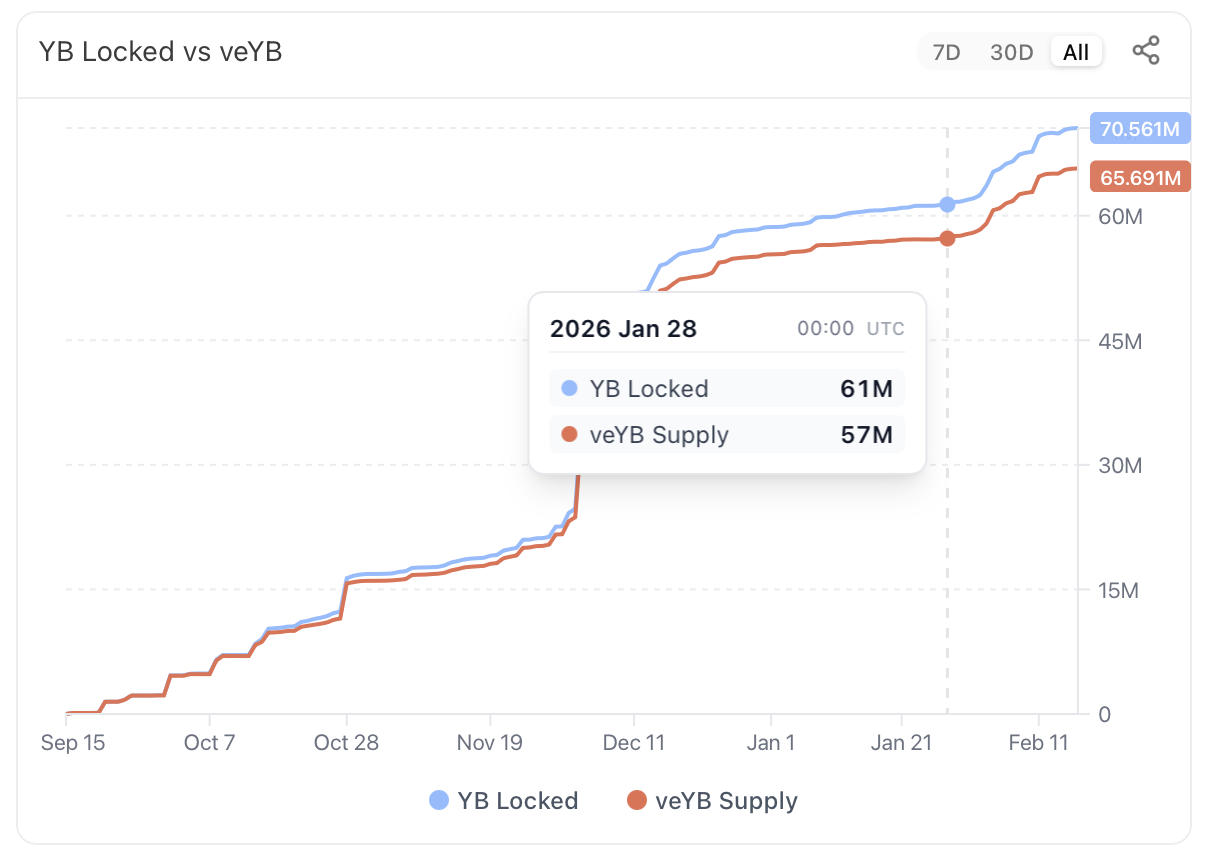

This was reflected in increased veYB locks (61M -> 70.56M YB was locked to earn protocol fees):

One of crucial questions for any protocol with ongoing token emission is fees vs. emissions efficiency or does protocol actually earn, and not just subsidise LPs?

Table 2. YB Emissions vs. captured fees analysis since v2 pools launch (12 Nov 2025)

| Period | Captured fees (LP + veYB) | Emissions (USD equivalent of $YB emissions calculated daily) |

|---|---|---|

| 12 Nov - 12 Dec, 2025 | 3.73M | 2.03M |

| 12 Dec 2025 - 12 Jan 2026 | 1.31M | 1.99M |

| 12 Jan 2026 - 12 Feb 2026 | 7.11M | 1.29M |

| Sum | 12.15M | 5.31M |

| Difference (fees - emissions) | +6.84M |

It means that during all market periods (volatile and non-volatile ones) Yield Basis earned $6.84M of profit (fees after subtracting emissions cost) for LPs and veYB holders combined.

It is a truly outstanding result for emerging Defi protocol during the first months of operating taking into account that these months have the highest inflation rate. Every following month YB emission is algorithmically reduced.

Upcoming updates to decrease YB influence on the $crvUSD Peg

Swaps in Yield Basis pools influence $crvUSD peg since every arbitrage or liquidation swap $BTC->$crvUSD requires further conversion $crvUSD -> $USDT/$USDC in corresponding Curve pools. It means constant pressure on $crvUSD peg during the $BTC downtrends.

Scaling Yield Basis to multi-billion TVL requires enhanced peg stability and reduced $crvUSD sensitivity to protocol-triggered $crvUSD swaps, which has led to a series of governance proposals.

Table 3. Proposals focused on enhancing $crvUSD peg stability and ensuring safe Yield Basis scaling.

| Proposal | Description |

|---|---|

| Yield Basis proposals | |

| Reduce stablecoin allocation for all BTC markets for safety of crvUSD, before HybridVaults | Executed: Reduce stablecoin allocation to 2/3 of current value for WBTC, cbBTC, tBTC markets Implication for the $crvUSD peg: this proposal cut TVL cap of BTC pools by 33% without necessity to withdraw $BTC by LPs. Such an option became available due to the $BTC price decline. Execution of this proposal directly decreases YB-related $crvUSD selling pressure exposure by 33%. |

| How to scale Yield Basis and crvUSD at the same time | Proposed: - launch a Hybrid Vault primitive, requiring deposit to $crvUSD Savings to unlock a personal TVL cap for YB LP, based on proof of peg support. Additional read on Hybrid Vault - add volatility tax charged from veYB admin fees stream in case of significant BTC pools disbalance (40/60 or more downwards) and use this tax proceeds as incentive for $crvUSD Savings. - pools optimizations that will make YB Pools earnings more uniform Implication for the $crvUSD peg: - Hybrid Vault: the new TVL deployed to Yield Basis pools will have necessary $crvUSD peg protection measures as an entry requirement - Volatility tax: during periods of elevated volatility, the mechanism significantly increases $crvUSD Savings yields, incentivizing market participants to acquire $crvUSD and deposit it into the Savings Vault. This acts as a direct peg support mechanism. Our analysis indicates yields of up to ~40% APY during peak volatility weeks. - Pool optimisation is a kind of a synergistic improvement that increases LP/veYB revenue in case of better $crvUSD peg stability |

| Curve proposals | |

| Increase a max revshare of $crvUSD revenue from 50% to 80% | Proposed: update the $crvUSD revenue split between CRV DAO and scrvUSD: from 50/50 to 20/80 Implication for the $crvUSD peg: elevated yields in the $scrvUSD Savings Vault drive demand for $crvUSD and increase deposit flows, contributing to peg support. |

| Grant eDAO peg defending capabilities | Proposed: transfer 400k $crvUSD from DAO Treasury to eDAO balance. These funds are allocated to support $crvUSD peg during extreme volatility (provide additional incentives to $crvUSD Savings and PegKeepers pools). Implication for the $crvUSD peg: increased incentives for $crvUSD Savings in volatile periods drive deposits to $scrvUSD that support the peg, increased PegKeepers incentives increase their capacity for peg support. |

In addition to proposals targeting $crvUSD peg stability, a separate set of proposals focuses on increasing LP earnings & veYB fees during upcoming pools rebalance.

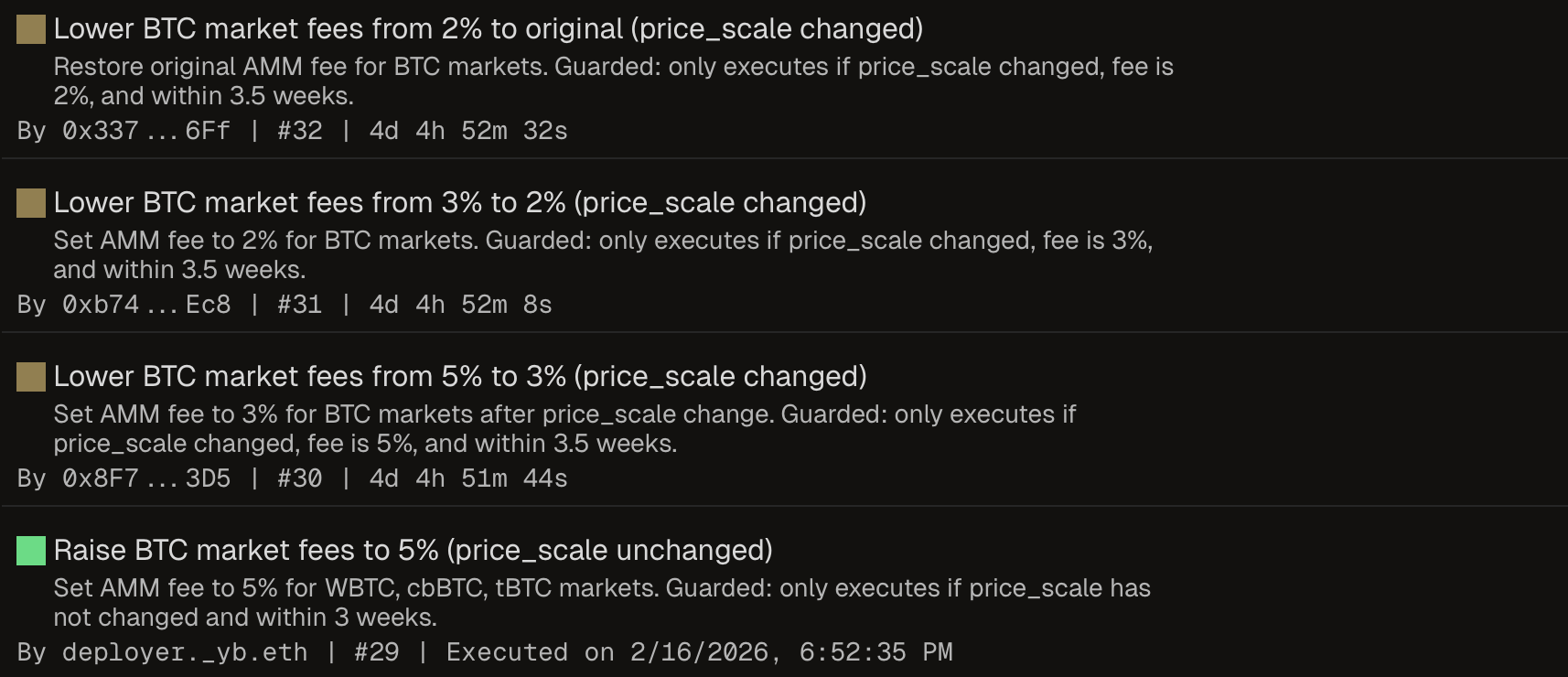

They are available at the YB governance section:

The first proposal increases the fee in LEVAMM to 5% (already executed) and then the following ones decrease it: 5% -> 3% -> 2% -> original fee.

Expected results of mentioned proposals implementation:

- Higher LEVAMM fees lead to a decreased loss of value by the LEVAMM during routine re-leveraging operations

- As a result, the regime in which admin fee accrual is temporarily disabled in order to recover losses sustained to re-leverage premiums is shortened

- Therefore, the YB LPs and veYB holders will receive generally higher and more consistent fee returns

We made a backtesting of Proposal #29 (5% fee) and our data confirms the theoretical explanation above.

Feedback appreciated

We are open to feedback on this research in Twitter DMs.

Disclaimer: This article and the accompanying analysis are provided by Valueverse for research and educational purposes only. All token valuation frameworks, metrics, comparisons, and conclusions discussed herein are experimental in nature and may rely on incomplete, estimated, delayed, or incorrect data, as well as subjective assumptions and methodologies.

The presented analyses do not represent definitive valuations, forecasts, or assessments of financial performance, and should not be interpreted as statements of intrinsic value. Digital assets and tokens are highly volatile, and their economic characteristics may change over time.

Nothing in this publication constitutes investment advice, financial advice, legal advice, or a recommendation to buy, sell, or hold any asset. Readers are solely responsible for their own research, risk assessment, and investment decisions.